Digital transformation begins not with technology, but with strategy. Too often, we hear the phrase “digital strategy” used as a justification for investing in new systems. While such investments are important, they must be rooted in the overall strategic positioning of the financial institution. Only with a clear business strategy can transformation unfold in the right direction, speed, and sequence.

Thanks to recent shifts in the broader fintech market, traditional financial institutions now have fresh opportunities to strengthen their positions. But there is no time to lose. Transformation requires urgency, clarity, and purpose.

The Core Functions of Financial Institutions

Before we consider digital transformation, let’s step back and remember the three fundamental economic functions of financial institutions, which have remained consistent over time:

1. Risk Management

Banks assess, price, and take risks, earning income (primarily interest income) in return. Despite new entrants such as direct lenders, this remains a central banking function.

2. Liquidity Bundling and Brokerage

Banks collect deposits of different sizes and maturities, bundle them, and provide loans in amounts tailored to client needs.

3. Maturity Transformation

Banks transform short-term deposits into longer-term loans, enabling borrowers and depositors to pursue plans independently of each other.

Digital transformation, when aligned with these functions, offers enormous potential to redefine how financial institutions deliver value.

A Strategic Foundation for the Future

While even at Q-Lana, we support financial institutions worldwide with our low-code-based, digital lending, and asset management platform, technology is only part of the story. A successful business strategy for the future of banking must rest on two pillars:

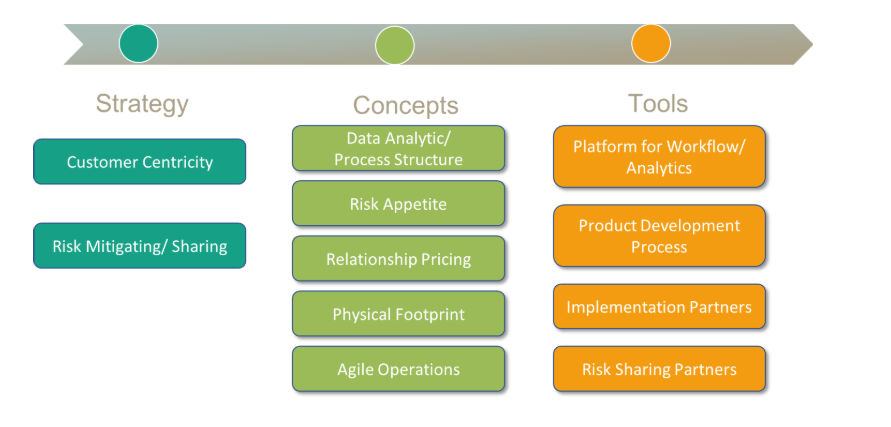

1. Customer-Centricity

Long-lasting client relationships provide proprietary knowledge that is an institution’s greatest competitive advantage. A customer-centric approach uses this knowledge to design individualized products, build loyalty, and reduce risk. Done well, it creates mutually beneficial relationships that increase revenues, lower costs, and strengthen margins.

2. Structured Risk Management

Local and regional institutions are uniquely positioned to understand client risk through personal interaction and trust. By structuring this knowledge, using methodologies to calculate Probability of Default (PD), Loss Given Default (LGD), and Early Warning Systems (EWS), institutions can not only manage risk more effectively but also unlock opportunities for risk-sharing with investors.

Supporting Concepts for Strategy Execution

To bring customer-centricity and risk management to life, several concepts must be embedded into the institution’s structure and operations:

Data Analytics

- Effective use of data requires governance, integration, quality assurance, secure storage, and analytics tools. Institutions must also invest in skills, infrastructure, and executive buy-in.

Process Structure

- Standardized processes (acquisition, data collection, approval, monitoring, collection) ensure efficiency, comparability, and scalability across all products.

Risk Appetite

- A dynamic risk appetite framework streamlines exposure management by setting limits per counterparty, enabling flexible approvals, and enhancing transparency.

Relationship Pricing

- Moving beyond static pricing tables, institutions can use models such as Risk-Adjusted Return on Capital (RAROC) to calculate revenues and costs across an entire relationship. This allows for flexible, dynamic, and mutually beneficial pricing.

Optimized Physical Footprint

- Branch networks must evolve into tech-enabled hubs, combining digital tools with advisory services. Outlets can be multifunctional, providing financial services, co-working spaces, or digital experiences.

Agile Operations

- Transformation requires agile working methods, prioritizing speed, flexibility, and cross-functional collaboration over rigid structures.

Workflow and Analytics Platforms

- Beyond core banking software, institutions need platforms to manage workflows, decisions, client interactions, and monitoring. These platforms should integrate CRM, document management, risk engines, ESG metrics, and open APIs. Q-Lana is designed precisely for this role.

Product Development Processes

- Personalized products demand faster innovation cycles. Agile methods allow institutions to move from idea to launch quickly, responding to constant demand for innovation.

Partnerships for Success

No institution can transform in isolation. Partnerships play a critical role:

Implementation Partners

Experienced advisors and technology providers help institutions execute transformation efficiently, avoiding pitfalls.Risk-Sharing Partners

Collaboration with investors and fund managers enables institutions to share risks, attract capital, and strengthen resilience.

At Q-Lana, we established Q-Lana Investment Advisors to prepare an SME Lending Fund for precisely this purpose.

Developing a business strategy is the cornerstone of digital transformation. By centering on customer-centricity, structured risk management, and enabling concepts, institutions can create a sustainable and competitive model. Technology, platforms, and partnerships then bring the strategy to life.

What’s Next in the Series

In the next chapters of our series, we will dive deeper into specific components of this strategy, such as customer-centric models, risk management frameworks, and data analytics, to demonstrate how to build a truly modern financial institution.