In the last session, we covered the details about customer centricity. Well implemented concepts of customer centricity will also lead to reduced risks. In the session of the blog about the business plan, we will explain that a financial institution is in a unique position to measure and manage risk, especially credit risk.

Banks’ Unique Advantage in Understanding Risk

Banks, in particular, local and regional institutions, were always in the privileged position to create and collect proprietary knowledge about their customers. Admittedly, not many used that privilege in a structured manner. Through personal interaction, long-term relationships, and a thorough understanding of the environment, relationship managers in financial institutions are generally better positioned to understand risk. Through their proximity to clients, familiarity with local procedures, and the trust they created with their customer-centric approach, banks are also the best equipped for collection and special servicing. To capitalize on those advantages, the bank shall establish the methodologies for assessing risks. We will introduce the key components of risk management in this blog.

The Foundations of Risk Management in Financial Institutions

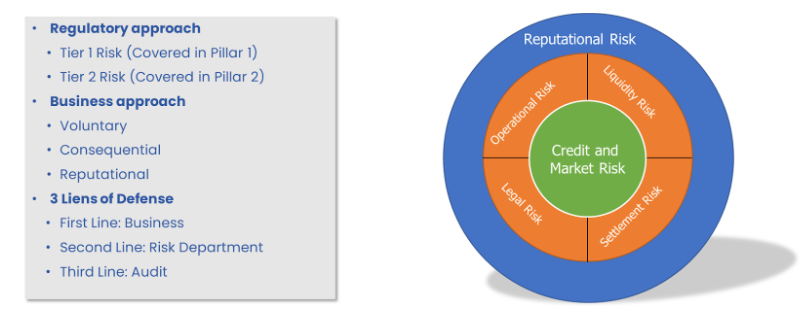

Risk management is a crucial facet of the operations of any financial institution. It encompasses a range of strategic components designed to assess, mitigate, and navigate potential uncertainties. From a regulatory perspective, the main categories of risk are related to credit, market, and operations. For the business plan which we discuss here, we focus on credit risk.

Focus on Credit Risk

Credit risk is a voluntary risk, meaning, it is a risk that the institution has the liberty to accept or decline. Credit risk is also very much the focus of the first line of defense in risk management in an institution, which requires that transparent and well-analyzed information has to be available to the front office. I know, there is a lot of jargon and background. We try to stay focused on the key items. In parallel, we are also preparing several online seminars and training sessions about risk management that you will find on our website.

The Concepts of Credit Scoring and Rating Models

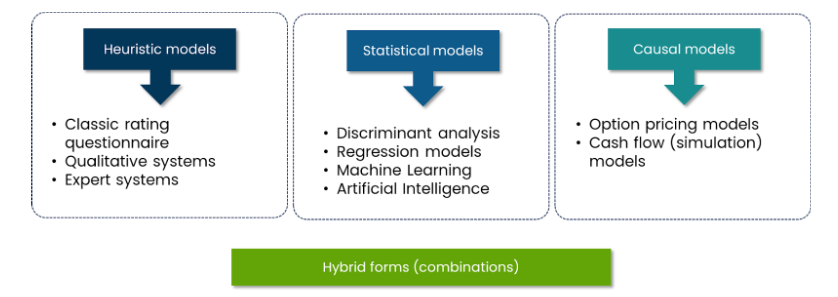

To manage credit risk, we need to combine tools, skills, and experience with proprietary knowledge about the customers and local markets. Sources of information are broad if not unlimited. They can be classified as quantitative and qualitative, or external and internal. The key is to identify the relevant sources for the assessment of credit risk. In this context, you hear about rating and scoring models. They aggregate information about credit risk into a single number, a score. This score shall classify the exposure on a risk scale. This is an attempt to structure the approach to credit risk. Depending on the nature and size of a counterpart, the calculation of a score can be more or less complex. A lot of myths rank around scoring models and their quality.

When you hear conversations about those models, there are frequent references to Machine Learning, AI and other technologies.

Let’s try to unpack the tools:

Scoring Models for Retail Borrowers

- The simplest form of scoring is often used for retail/mass market borrowers who do not yet have a client relationship. Here external information, including demographic data or assessments provided by credit bureaus is used. In more developed countries, instruments like a FICO score are well established. While the exact formula for the calculation of a FICO score is secret, we know the input factors, which are a person’s payment history, amounts owed, length of credit history, new credit accounts, and types of credit used.

- Once an institution has established a lending relationship, the calculation of the score can get more sophisticated as real payment performance and transaction data can be used to enrich the calculation. Such scores help an institution scale the credit exposure or offer additional products to a client.

Scoring Models for SMEs and Corporate Clients

- Once you come to larger clients, specifically for SMEs and Corporates, the calculation of a score gets more complex, as more qualitative information needs to be taken into consideration. The question of whether an SME as a counterpart defaults depends on the company’s financial strength, but also on factors such as the management’s skills and experience in managing crisis situations. Ratings for such customers will rely to an increasing degree on heuristic concepts, combined with statistical methods.

Rating and Scoring Require Ongoing Monitoring

- Rating and scoring are not just used for an initial assessment of credit quality, but also for monitoring and valuation. In retail, a lending decision is often considered as an educated bet on a client’s performance. For corporates and SMEs though, a proper monitoring process that also includes rating updates can be essential to interfere early with a borrower’s operation to avoid later performance problems.

While rating and scoring models are rather common and standard, we still think that financial institutions can increase the predictive quality of a model by increasing the variety of input factors. One area where we believe more information will contribute to the model quality is the whole area of ESG risk assessment. Integrating this source of information will be invaluable.

An interesting component of all these scoring models is the ability to make credit risk comparable.

Here, a standardization regarding the measurement is suggested. Ideally, a financial institution attempts to derive a Probability of Default from a rating or scoring model. This is a commonly defined indicator for credit risk. It differentiates itself from the Loss Given Default, which measures the quality of the collateral package and predicts how much a financial institution will lose assuming that the client reaches a default stage. Together with the exposure at default, the three factors allow the calculation of the expected loss.

In a later chapter, when we talk about the risk appetite, we will pick up on the calculation of the expected loss again.

Improving Ability to Measure and Manage Risks

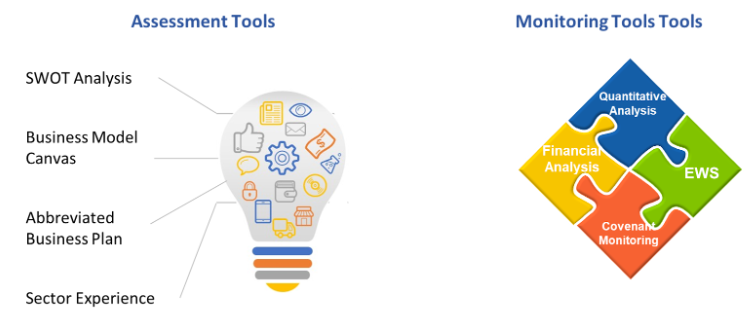

Aside from standardized rating and scoring models, we think that financial institutions can also improve their ability to measure and manage risks through upgrades to the overall lending process. This starts with the assessment of credit risk where tools, such as a SWOT analysis, an abbreviated business plan, sector expertise, or tools, such as the business model canvas, will help structure the credit risk assessment. The key here for a financial institution is to fully understand a customer’s business and the inherent risks. This sounds trivial on the surface but is more complex than appears. Improvements to the lending process can be made in all phases. This relates to better assessment during the assessment and analysis phase, better tools to reduce the operational and fraud risks, and structured monitoring which helps identify problems early on.

The Role of Monitoring and Early Warning Systems

Having a monitoring and early warning system in place as well as structurally enforcing the necessary steps on borrowers is useful.

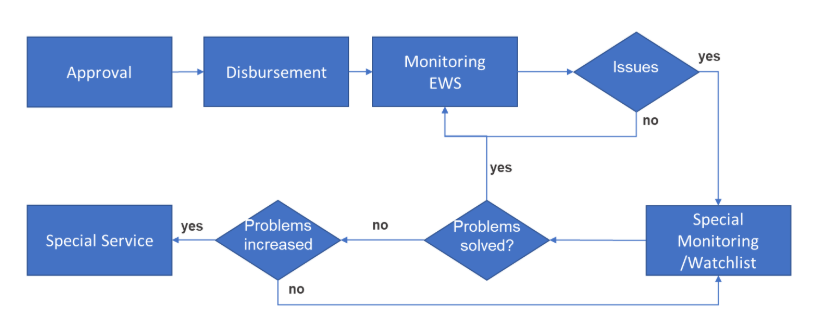

A financial institution shall focus on the monitoring of the borrowers right after the disbursement. This includes the process of regular monitoring of performing loans. A process such as the one shown here is useful. We still see too many institutions which do not and bother to work with the customer if debt service payments occur. An institution will never develop a positive and fruitful client relationship if the only contact with the client after disbursement is happening when problems arise. Specifically in the area of corporate and SME lending, relationships are formed when the client recognizes that the institution cares about the positive performance of the business.

Benefits for Both Institution and Borrower

One of the benefits we often discover in institutions where such client relationships are actively maintained is that borrowers even approach the institution in case of problems.

Early warning systems that incorporate regular quantitative analysis of external and internal indicators, covenant monitoring, financial analysis, as well as early warning questionnaires, count as best practices for monitoring.

With an effective Early-Warning System (EWS), credit losses are reduced through de-risking. By the way, this will also improve the institution’s capacity to take risks, increase returns and improve capital productivity. For the client, the benefits include lower pricing as well as the active support from a qualified expert in the management of critical situations.

Even in this short introduction, you can already see that with a well-structured setup of risk management, the bank is in the position to price the risk and provide confidence to investors about its ability to measure and manage risks. This opens the door to selling parts of the risks to investors, for example through risk-sharing funds, while maintaining the responsibility for servicing and collecting. This is useful because of a critical aspect: while a financial institution can be strong in measuring and managing risks, it might not be in the best position to assume all the risks. A financial institution that is focused on capitalizing its unique knowledge for the generation of revenues, minimizing risk, and optimizing the utilization of its equity capital will be a winner.

What’s Next in the Series

In the next session of the blog we will speak about Data Analytics, another core concepts that support a financial institution’s business model.