Data analytics has become one of the most important topics for financial institutions today. Banks and asset managers sit on an enormous wealth of data, and the question is no longer whether to use it, but how to structure, analyze, and apply it effectively.

Done well, data analytics lets you know more about customer behavior, market dynamics, and operational performance. It allows institutions to make better decisions, anticipate risks, and design innovative products. In short, it transforms raw data into a competitive advantage.

What is Data Analytics?

At its core, data analytics is the process of examining large volumes of raw data to extract meaningful insights, patterns, and trends. These insights help institutions make better-informed decisions, optimize operations, and strengthen customer relationships.

Data analytics not only supports the financial institution itself but also enables collaboration with partner institutions, regulators, and investors.

Key Components of Data Analytics

To build an effective analytics function, financial institutions must structure their work around five key components:

1. Data Collection

Gather relevant information from multiple sources: internal (transaction records, customer accounts, operational data) and external (market indicators, economic statistics, social media). Accuracy, security, and compliance with privacy regulations are essential.

2. Data Cleaning and Preparation

Raw data is messy. Errors, inconsistencies, and missing values must be addressed. Clean, structured data is the foundation for reliable analysis.

3. Descriptive Analytics

Use statistics and visualization tools to summarize past performance and customer behavior. Descriptive analytics answers the question: What happened?

4. Diagnostic Analytics

Go deeper to uncover the why. Root cause analysis identifies the drivers behind outcomes such as revenue fluctuations, customer churn, or fraud events.

5. Predictive and Prescriptive Analytics

Predictive: Forecasts future events and behaviors using historical data and statistical models.

Prescriptive: Suggests optimal actions based on insights, such as recommending portfolio adjustments, identifying high-risk accounts, or tailoring loan offers.

Applications of Data Analytics

When implemented properly, data analytics strengthens institutions across multiple areas:

Informed Decision-Making: Replace intuition with evidence-based insights.

Risk Management: Identify patterns that signal credit, market, or operational risks.

Customer Insights: Understand behavior, preferences, and needs to build personalized solutions.

Process Optimization: Detect inefficiencies and reduce costs by streamlining workflows.

Compliance & Fraud Detection: Spot anomalies to ensure regulatory compliance and prevent fraud.

Innovation & Growth: Use trend analysis to identify opportunities for new products, partnerships, or services.

Structural Considerations

Building a strong data analytics function requires more than technology. It is a strategic initiative with organizational, cultural, and regulatory dimensions.

1. Data Governance and Management

Establish policies to ensure accuracy, consistency, and security. Compliance with frameworks such as GDPR is mandatory.

2. Integration of Data Sources

Connect customer, transaction, market, and economic data into a single ecosystem for unified analysis.

3. Data Quality Assurance

Implement ongoing quality checks to maintain reliability. Poor data leads to poor decisions.

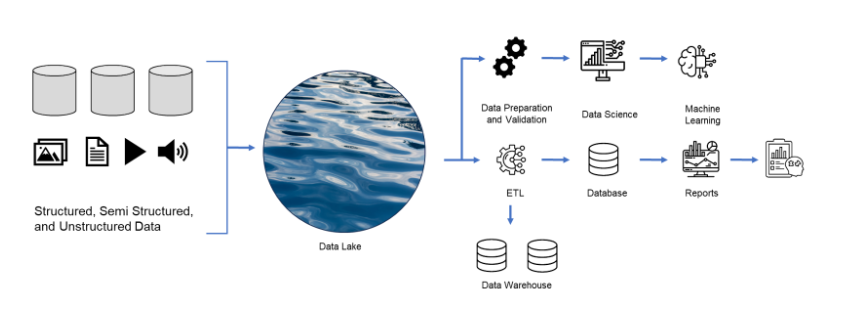

4. Data Warehousing and Data Lakes

Create scalable repositories for both structured and unstructured data. Ensure flexibility to adapt to new sources and larger volumes.

5. Team Structure and Skills

Build cross-functional teams that include data scientists, engineers, business analysts, and domain experts. Balance technical skills with business knowledge.

6. Data Security and Privacy

Protect sensitive data with strong security protocols. Use anonymization where appropriate.

7. Collaboration Across Departments

Finance, risk, marketing, and IT must work together to maximize the impact of analytics.

8. Executive Buy-In

Senior management must provide resources, budget, and visibility to make analytics a strategic priority.

9. Training and Data Literacy

A culture of data-driven decision-making requires training staff across all levels of the institution.

10. Scalability and Adaptability

Systems must be designed for growth—both in data volume and in complexity of analysis.

What’s Next in the Series

Data analytics is not just a technical project—it is a strategic capability. By structuring analytics carefully, financial institutions can build customer-centric solutions, improve risk management, and create sustainable growth.

At Q-Lana, we combine expertise in risk, customer-centric banking, and digital platforms with dedicated data analysts and architects. This enables us to support institutions in structuring their data analytics strategy and turning insights into action.

In the next chapter of this series, we will discuss the concepts of Risk Appetite and Relationship Pricing—two powerful tools for linking customer-centric strategies with structured risk management.