An essential part of the business model is the ability to share risks with investors. To approach these sources of risk capital, the financial institution shall work with one or more funding providers or find managers on the concept of risk sharing. A fund manager can launch targeted open-ended and closed-ended investment funds to reduce the risk from loan exposures for the financial institution. Such a funding provider will also provide advice on the proper structuring and pricing of assets that are earmarked for selling.

Introducing the SME Lending Fund

In this final chapter of the block series on digital transformation and business strategy, we would like to introduce to you the concept of the SME lending fund, which we have developed over the past years at Q-Lana, and are planning to launch together with our own asset management subsidiary, Q-Lana investment advisors.

Providing financial services to SMEs is among the most interesting and most challenging business areas for traditional financial institutions. Financial services for SME clients require specific understanding of the way those companies conduct business, the entrepreneur’s personality, strengths, and weaknesses.

Providing Financial Services for SME Clients is for the Largest Part Relationship Banking

It can take several years to build an understanding of the client and the business potential. A good SME relationship manager in a financial institution has gained the trust of the entrepreneur and of the management of the company. The relationship manager fully understands the business of the client and the personality of the people involved.

Successful financial institutions in the SME space build up this understanding and knowledge through a strong focus on the interaction with the client. Entrepreneurs on the other hand value both solid and modern financial services as well as a trustful relationship with their financial institution. They prefer to rely on a financial institution as a long-term business partner, based on trust and understanding. The local presence and the proximity to the SMEs puts local financial institutions in an advantageous position when it comes to monitoring and collecting on loans.

Linking Back to Business Strategy

The entire Business Strategy which we presented in this blog series is based on this concept of customer centricity and proprietary knowledge in the assessment and management of risk.

SME Loans Attract Investors

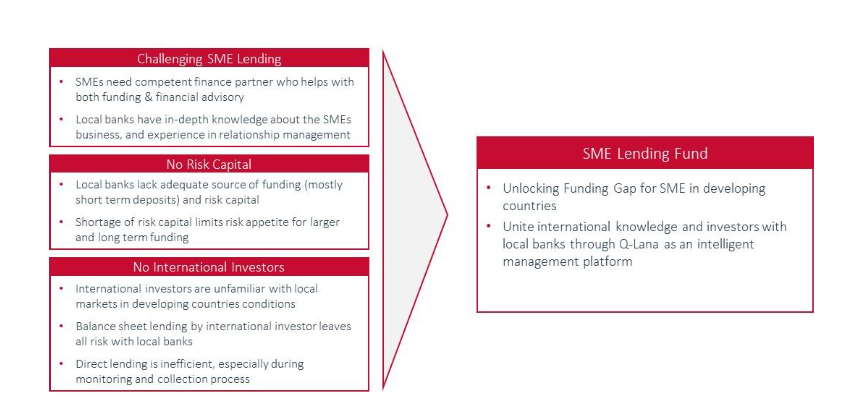

Loans to local SMEs are an attractive asset class, to which domestic and international investors usually have no access. In general, the lending requirements of established banks are thorough, including enforceable collateral. Interest rates are attractive and SME loans usually do not correlate with other established asset classes. Currently, investors barely have access to those loans. International financial institutions and development financial institutions often provide loans to larger banks for balance sheet lending. This does not create direct exposure to the SME loans, since defaults are digested by the local banks. Investing in international funds, including traditional impact investment funds does not provide sufficient yield, since the operating costs of such funds are high.

The SME Lending Fund Solution

The SME Lending Fund addresses the issues described in the previous section and provides an attractive solution at a low cost. It solves the challenges of SME lending by combining the strengths of the existing local banks and investors. In this model, local financial institutions are the competent finance partners to SMEs, providing both funding and financial advisory. This leverages the in-depth knowledge about SMEs, accumulated by the local banks.

How the Fund Works

The lack of risk capital of local financial institutions is addressed through a risk-sharing mechanism through which the SME lending fund, and ultimately the investors, takes actual default risk and the underlying loans, reducing the requirements for local banks regarding regulatory capital and providing a solution to the gap in term funding:

- By collecting funds from international and domestic investors and investing them in loan participations, originated by local financial institutions, investors have direct access to the credit risk, while leaving the origination and monitoring to the local institution.

- By engaging in a risk-sharing mechanism through arrangements like silent participations or club transactions, the interest in monitoring the loans and collecting outstanding amounts is aligned between the financial institutions and the investor.

General Structure

The general structure of the SME Lending Fund is shown in the following description. The structure is based on a complex version that allows for fundraising in international markets.

Wrapping Up the Series

We have now come to the end of this series on Digital Transformation and Business Strategy. Over the past chapters, we explored how financial institutions can combine customer-centricity, structured risk management, data analytics, and innovative partnerships to strengthen their business models.

Risk sharing, as we discussed here, is a vital element that connects institutions with investors and creates resilience in SME lending. At Q-Lana, we are committed to helping financial institutions put these strategies into practice.

Thank you for following along with us in this series. We look forward to continuing the conversation and supporting you on your digital transformation journey.