Lack of comprehensive data makes credit assessments challenging. This is evident when evaluating small and medium-sized enterprises (SMEs), which often operate with limited financial disclosures and inconsistent reporting. In such cases, it is important, as a lender, to look beyond your traditional financial statements and clearly understand your borrowers true potential and risk exposure. What SWOT analysis really tells you about SME borrowers is that it provides a structured framework to fill these information gaps, helping lenders make more confident and informed decisions.

What is SWOT Analysis?

The Chartered Institute of Personnel and Development (CIPD) defines SWOT analysis as,

A planning tool which seeks to identify the Strengths, Weaknesses, Opportunities and Threats involved in a project or organization. It’s a framework for matching an organization’s goals, programs and capacities to the environment in which it operates.

SWOT analysis is a strategic planning tool that identifies internal and external factors that can impact a business. It is a structured approach that enables you, as a lender, to bridge information gaps, especially when dealing with SMEs. It aligns your credit strategies with a borrower’s real-world conditions.

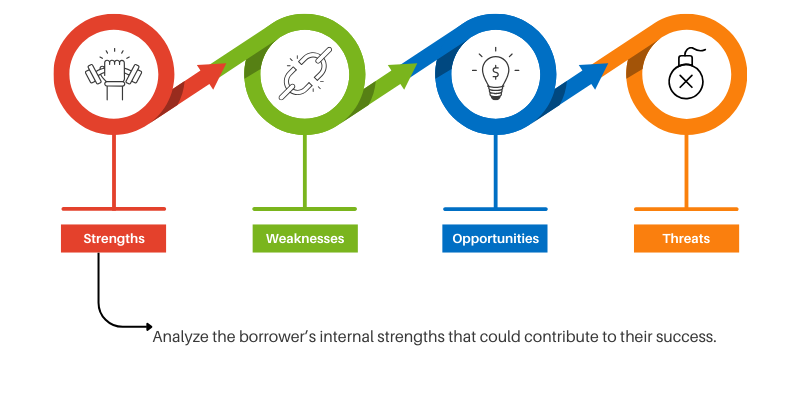

The framework is divided into four components:

Components of SWOT Analysis

1. Strengths of SME Borrowers

Strengths are what make an SME stand out. SMEs could have a loyal customer base, niche market expertise, or innovative products. These attributes enhance their chances of securing loans and indicate potential for profitability.

A well-managed cash flow, strong management team, and strategic location can also give SMEs an edge. These strengths are crucial for lenders to see beyond the balance sheet and recognize the potential for growth.

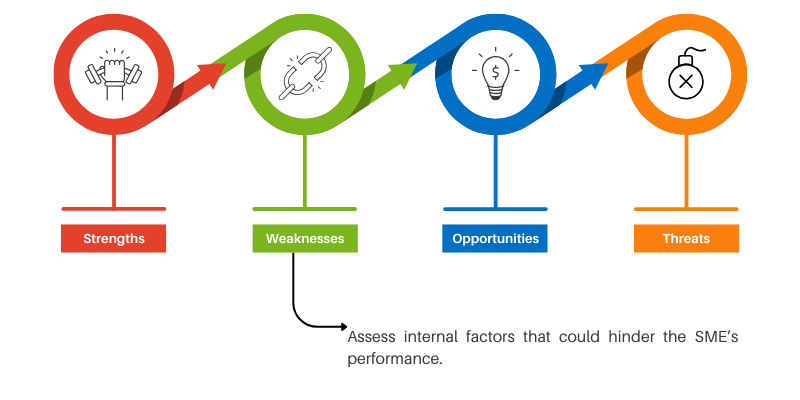

2. Weaknesses of SME Borrowers

Weakness can include limited access to capital, outdated technology, or high debt levels. No one likes to think about their flaws, but acknowledging these weaknesses is essential for both SMEs and lenders. Therefore, as a lender, you can tailor your financial products to fit the needs of the borrower. That also entails working towards minimizing any risks associated with the loan.

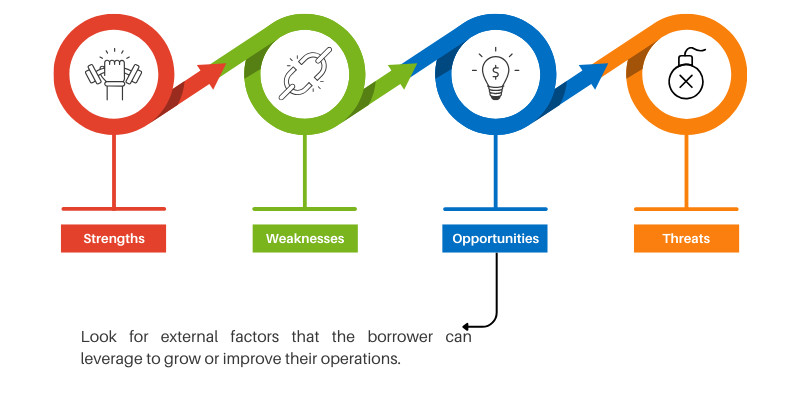

3. Opportunities for SMEs in Borrowing

SMEs are always looking to borrow, and opportunities are unlimited. Today, there is a rise of digital banks, alternative lenders, and government initiatives, all designed to support SMEs. This means that there are more options to funding than ever before. Additionally, economic trends such as increased consumer demand or new market gaps can be catalysts for growth. By leveraging these opportunities, SMEs can position themselves for success while lenders can feel more confident in the potential for financial returns.

4. Threats Facing SME Borrowers

Every silver lining has a cloud, and for SMEs, threats can come from various angles. Increased competition, economic downturns, or shifts in consumer behavior can all pose risks to an SME’s borrowing capability. Identifying these threats is crucial for lenders, as it allows them to foresee challenges that could hinder repayment and to devise strategic support to navigate them.

SWOT analysis enables financial institutions to understand an SME borrower’s current position and future potential. This understanding enables better credit assessments.

SMEs and Their Borrowing Needs

Many SMEs face significant obstacles when trying to access formal financing.

Common barriers include:

limited credit histories

insufficient collateral

informal financial records

volatile cash flows, etc.

All the above make traditional credit assessment methods very ineffective.

What SWOT analysis really tells you about SME borrowers at this stage is how their real borrowing needs connect to both internal challenges and the external market environment.

SWOT as a Modular Credit Tool

SWOT analysis entails several steps that contribute to comprehensive and accurate results:

1. Preparation and Data Collection

Gather relevant information about the SME borrower. This includes:

Financial statements

Market research

Industry reports

Customer feedback, etc.

Engaging with the borrower directly can also contribute a lot to their operations, goals, and challenges.

2. Identify Strengths

These might include:

Strong cash flow and profitability

Established customer base

Skilled management team

Unique products or services

Pay attention to indicators of financial stability, such as positive cash flow and a low debt-to-equity ratio, recognizing that much of this information may come from informal sources, such as “back of the envelope” assessments rather than official financial statements. These informal indicators can provide valuable insights into a borrower’s true financial health, especially in contexts where formal documentation is lacking.

3. Identify Weaknesses

Common weaknesses include:

Poor financial management

Limited market presence

High employee turnover

Outdated technology

Understanding these weaknesses helps lenders anticipate potential risks and work with borrowers to address them proactively.

4. Identify Opportunities

Opportunities might include:

Expanding into new markets

Launching new products or services

Benefiting from regulatory changes

Accessing government grants or subsidies

Financial institutions can support borrowers by identifying opportunities that align with their strengths and strategic goals.

5. Identify Threats

These threats might include:

Recognizing potential threats enables financial institutions to better assess the borrower’s resilience and risk management capabilities.

6. Develop an Action Plan

The final step is to create an action plan based on the SWOT analysis findings. The plan should address weaknesses and threats while leveraging strengths and opportunities. Financial institutions can collaborate with borrowers to develop strategies for improvement, such as financial restructuring, operational enhancements, or market expansion. Additionally, the findings from a SWOT analysis can be used to train loan officers, enhancing their ability to conduct future assessments.

Benefits of SWOT Analysis in SME Lending

SWOT analysis offers several advantages for financial institutions when assessing SME borrowers:

Challenges of SWOT Analysis in SME Lending

Even with its benefits, what SWOT analysis really tells you about SME borrowers can be incomplete if data is missing, biased, or oversimplified.

i. Subjectivity

SWOT analysis relies on qualitative data, which can be subjective and prone to bias. Involving multiple stakeholders and using objective data sources can help mitigate this risk.

ii. Incomplete Information

If the borrower fails to provide accurate or comprehensive information, the analysis may be flawed. Lenders should verify data through third-party sources where possible.

iii. Overlooking Interconnected Factors

Strengths and weaknesses can be interconnected, and opportunities may carry inherent risks. Lenders must consider these nuances to avoid oversimplifying the analysis.

iv. Time and Resource Intensive

Conducting a thorough SWOT analysis requires time and resources. Financial institutions must balance the depth of analysis with operational efficiency.

Empowering Credit Assessment with Q-Lana’s SWOT Integration

SWOT is a fast and efficient way to compare companies operating in similar sectors. Identifying strengths, weaknesses, opportunities, and threats gives lenders a clearer picture of a borrower’s current position and future potential. Moreover, SWOT analysis results are useful in better understanding of the credit risk profile of the borrower.

SWOT analysis has challenges, not doubt. But the benefits far outweigh the drawbacks when it comes to making informed lending decisions and fostering long-term relationships with SME clients.

SWOT analysis, when integrated into your credit evaluation workflow, enables you to create of stronger and ultimately more profitable lending portfolio.

At Q-Lana, we have embedded SWOT into our Loan and Asset Management Platform, and this has made the tool powerful, readily accessible and easy to use.