Credit risk is the most critical risk category for any lending-focused financial institution. It underpins a wide range of financial activities, from traditional term loans and complex structured finance to trading products. A solid understanding of credit risk is essential for accurate pricing, effective portfolio management, and overall institutional resilience.

Over time, financial institutions have developed diverse methodologies to assess credit risk. These range from straightforward scorecards based on a handful of indicators to in-depth, multi-page assessments incorporating comprehensive financial modeling. While the analytical foundations of these approaches are addressed in other publications, this series focuses on Credit Risk Modeling—the quantitative framework that builds on credit analysis and supports pricing decisions, capital planning, and strategic steering.

This Concept Note provides a structured, step-by-step exploration of the key components of credit risk modeling.

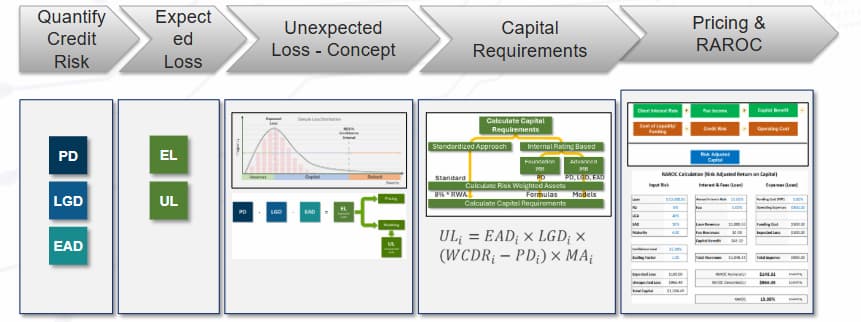

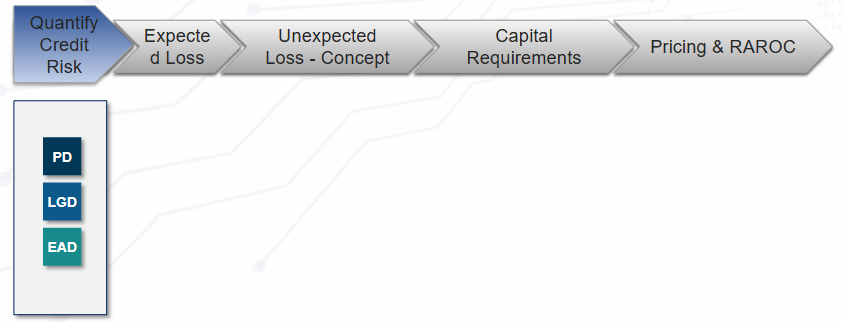

Chapter 1: Quantifying Credit Risk

This chapter of the credit risk concepts explains the three core variables:

i. Probability of Default (PD)

ii. Loss Given Default (LGD)

iii. Exposure at Default (EAD)

These variables form the foundation for all credit risk measurement and modeling.

Chapter 2: Expected Loss

This chapter covers the definition, calculation, and application of Expected Loss (EL). We also emphasize the role of expected loss in provisioning, pricing, and portfolio monitoring.

Chapter 3: Unexpected Loss

In this chapter, we explore Unexpected Loss (UL) in terms of how it is modeled using simulations, its role in capital adequacy, and why it is critical for absorbing shocks beyond expected defaults.

Chapter 4: Capital Requirements

Capital requirements link credit risk modeling to regulatory frameworks (Basel I–IV). The chapter details how financial institutions can calculate capital needs at the individual loan level using standardized and internal models.

Chapter 5: RAROC

In this final chapter of our credit risk series, we introduce to you Risk-Adjusted Return on Capital (RAROC).

We explain how financial institutions can align profitability with capital efficiency, using risk-adjusted metrics for loan pricing and strategic steering.