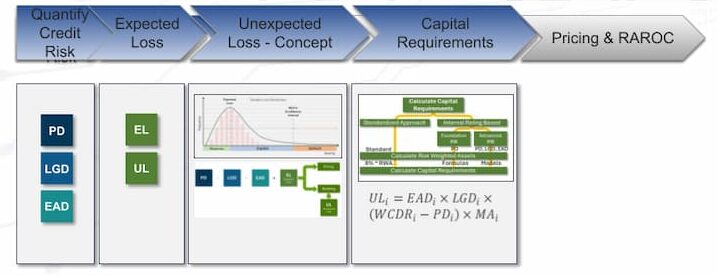

In previous chapters, we introduced the concepts of Expected Loss (EL) and Unexpected Loss (UL) and explored how these metrics can be modeled and quantified at the portfolio level. Now, we turn to the next logical step: quantifying capital requirements at the individual loan level.

This chapter explains how institutions can translate portfolio-level insights into loan-specific capital allocation, aligning credit risk sensitivity with pricing, portfolio strategy, and regulatory compliance.

Importance of Individual Loan Analysis

Calculating capital requirements at the individual loan level is critical for precision in credit risk management. It allows financial institutions to assess and allocate capital more effectively, ensuring that risk-sensitive pricing, portfolio optimization, and regulatory compliance are all achieved. By understanding the unique risk characteristics of each loan, institutions can tailor their strategies to balance profitability and risk exposure.

This will support several concepts:

i. Risk-Based Pricing:

Institutions can price loans more accurately by reflecting the specific risks of each borrower or transaction.

ii. Granular Risk Management:

Identifying high-risk loans within a portfolio enables targeted strategies, such as enhanced monitoring or adjusted collateral requirements.

iii. Regulatory Compliance:

Many frameworks, including Basel guidelines, emphasize capital adequacy at both the portfolio and individual loan levels.

iv. Enhanced Portfolio Steering:

Aggregating individual loan-level insights enables institutions to make more informed decisions about portfolio composition and risk mitigation.

While financial institutions can develop proprietary risk models to calculate capital requirements, it is necessary to first review the regulatory frameworks for requirements and guidance.

Regulatory Frameworks for Capital Requirements

The Basel Frameworks, established by the Basel Committee on Banking Supervision (BCBS), serve as the cornerstone for global financial regulation. These frameworks are developed to strengthen the stability and resilience of financial institutions by setting uniform standards for managing risks, including credit risk, market risk, and operational risk. Importantly, the Basel Standards are generally guidelines, which are subsequently adopted and implemented by individual countries as part of their national legal or regulatory frameworks. This approach ensures flexibility for local adaptation while maintaining a consistent global regulatory baseline.

Evolution of Basel:

- Basel I (1988): Introduced the 8% capital ratio and risk-weighted assets (RWA)

- Basel II (2004): Added internal models and the three-pillar approach

- Basel III (2010): Strengthened capital and liquidity rules post-2008 crisis

- Basel IV (2023): Refined risk sensitivity, re-emphasized standardized approaches, and placed limits on internal model usage

Origins of the Basel Framework

The Basel Committee was established in 1974 by the Bank for International Settlements (BIS), headquartered in Basel, Switzerland. The primary aim of the BCBS is to enhance the quality of banking supervision worldwide. The committee does not have legal authority to enforce regulations but works collaboratively with national regulators to implement its guidelines.

The need for a global regulatory framework became evident after a series of banking crises exposed vulnerabilities in financial systems. Differences in capital adequacy standards across countries led to a lack of uniformity in risk management, creating opportunities for regulatory arbitrage. The Basel frameworks address these disparities by providing standardized guidelines for risk measurement and capital allocation.

Evolution of the Basel Frameworks and Their Role in Quantifying Capital Requirements

i. Basel I (1988): The Foundation

The Basel I Accord introduced the concept of capital adequacy, requiring banks to maintain a minimum level of capital relative to their risk-weighted assets (RWA). The framework established a minimum capital requirement of 8% and introduced a risk-weighting system for different asset classes. For example, loans to sovereigns or government entities typically had lower risk weights compared to corporate loans.

While Basel I laid the foundation for global banking regulation, its simplicity had limitations. It did not adequately address the complexity of modern financial products and failed to differentiate risk levels within asset categories.

ii. Basel II (2004): Enhancing Risk Sensitivity

The Basel II Accord built upon Basel I by introducing a more nuanced approach to risk measurement through its three-pillar structure:

- Pillar 1: Minimum Capital Requirements

Basel II allowed banks to use internal models to calculate capital requirements for credit, market, and operational risks. This included methods like the Internal Ratings-Based (IRB) Approach, enabling banks to assess Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD) for individual exposures. - Pillar 2: Supervisory Review Process

This pillar emphasized the role of regulators in reviewing banks’ internal risk assessments and ensuring they maintained adequate capital. - Pillar 3: Market Discipline

Basel II introduced disclosure requirements to enhance transparency, enabling market participants to assess the risk profile of banks.

While Basel II improved risk sensitivity, it relied heavily on internal models, leading to inconsistencies and vulnerabilities. It also underestimated systemic risks, which became evident during the 2008 Global Financial Crisis.

iii. Basel III (2010): Addressing Crisis Fallout

In response to the 2008 crisis, Basel III introduced measures to address systemic risks and enhance the resilience of financial institutions. Key features included:

- Higher Capital Requirements: Increased the quality and quantity of capital, with a focus on common equity tier 1 (CET1).

- Leverage Ratio: Introduced a non-risk-based leverage ratio as a backstop to prevent excessive borrowing.

- Liquidity Standards: Established the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR) to ensure short-term and long-term liquidity.

- Countercyclical Capital Buffers: Required banks to hold additional capital during economic upswings to absorb losses in downturns.

iv. Basel IV (2023): Refinement and Simplification

Although often referred to as Basel IV, this is an extension of Basel III rather than a standalone framework. It aims to reduce variability in risk-weighted assets (RWAs) by limiting the use of internal models and increasing reliance on standardized approaches.

Key changes include:

- Revised Standardized Approach: Enhanced risk sensitivity while maintaining simplicity.

- Output Floor: Capped the benefits banks could derive from internal models, ensuring their capital requirements are not significantly lower than those calculated using the standardized approach.

- Operational Risk Revisions: Replaced internal model approaches with a standardized method to calculate operational risk.

The Basel IV updates aim to strike a balance between complexity and consistency, ensuring that banks maintain sufficient capital while enhancing transparency and comparability across institutions.

Objectives of the Basel Frameworks

The Basel Frameworks aim to achieve the following objectives:

- Financial Stability: Reduce the likelihood of bank failures and systemic crises by ensuring institutions hold adequate capital and liquidity buffers.

- Global Consistency: Establish uniform regulatory standards to create a level playing field across jurisdictions, reducing opportunities for regulatory arbitrage.

- Risk Sensitivity: Encourage banks to align capital requirements with the underlying risks of their exposures.

- Market Discipline: Promote transparency and accountability by requiring disclosures that allow stakeholders to assess a bank’s risk profile and financial health.

- Resilience to Shocks: Ensure that banks can absorb losses and continue operations during periods of stress, thereby safeguarding the broader financial system.

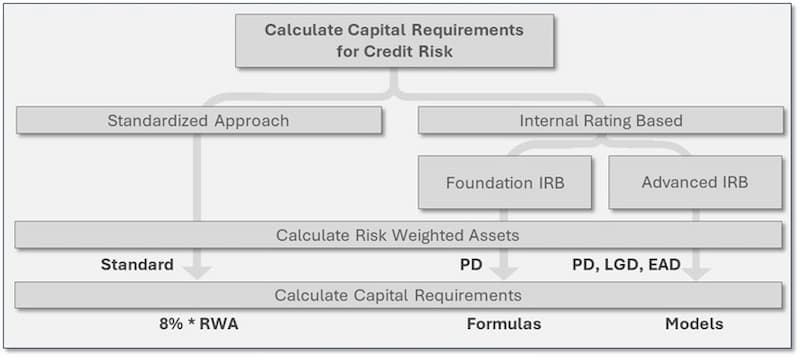

Basel’s Approaches to Credit Risk

The Basel Committee on Banking Supervision provides two distinct approaches to calculate credit risk capital requirements: the Standardized Approach and the Internal Ratings-Based (IRB) Approach. These frameworks are designed to ensure that financial institutions allocate sufficient capital to absorb potential credit losses while maintaining global stability within the financial system.

Standardized Approach:

Under the Standardized Approach, the Basel framework offers a simplified method for calculating risk-weighted assets. Financial institutions rely on risk weightings prescribed by regulators for specific asset classes or borrower types. This approach is straightforward and does not require banks to develop or use internal models. For example, loans to Small and Medium Enterprises (SMEs) may be assigned a uniform risk weight, regardless of individual borrower characteristics or differences in collateral. While the simplicity of this approach is advantageous for smaller institutions or those in developing markets, it often fails to account for nuances in risk levels associated with individual exposures.

Internal Rating-Based (IRB) Approach:

The Internal Ratings-Based (IRB) Approach, on the other hand, allows banks to use internal models to estimate credit risk. This method enables institutions to incorporate more granular data, improving the accuracy of capital requirements.

Foundation vs. Advanced IRB

The IRB Approach is subdivided into two categories: the Foundation IRB and the Advanced IRB.

- Foundation IRB

Under the Foundation IRB, banks estimate the Probability of Default (PD) for their borrowers but rely on regulator-provided values for Loss Given Default (LGD) and Exposure at Default (EAD).

- Advanced IRB

In contrast, the Advanced IRB allows banks to estimate all key components—PD, LGD, and EAD—using their internal models. However, the Advanced IRB requires rigorous validation by regulators to ensure the accuracy and reliability of the risk models.

IRB in the Basel Framework

The above two approaches, initially introduced under Basel II, remain foundational in Basel III and Basel IV, with adjustments to their applications. Basel IV, for example, places greater emphasis on the Standardized Approach, limiting the scope of the Advanced IRB for certain asset classes to address concerns about complexity and inconsistencies in model outputs. Nonetheless, the overarching concepts remain consistent, reinforcing the importance of aligning capital requirements with the underlying risks of loan portfolios.

Through both approaches, the Basel framework provides flexibility for banks to align their credit risk calculations with their capabilities and operational scale, ensuring that institutions, regardless of size, can meet regulatory standards while managing their risk effectively.

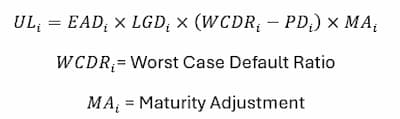

Formula for Individual Loan UL

For the next steps in our analysis, we will utilize the Foundation Internal Ratings-Based (IRB) approach outlined by the Basel regulatory framework. This approach offers financial institutions the flexibility to use their own internally estimated inputs, such as the Probability of Default (PD), while relying on standardized regulatory inputs for variables like Loss Given Default (LGD) and Exposure at Default (EAD). It is a balanced methodology that provides the benefits of customization without requiring the development of highly complex internal risk models, making it a practical option for many institutions.

Unexpected Loss (UL) represents the variation in losses that exceed the expected losses. Under the Foundation IRB approach, the UL for an individual loan is calculated using the formula:

Breaking Down the Components:

i. Exposure at Default (EAD):

The amount expected to be outstanding at the time of default.

ii. Loss Given Default (LGD):

The portion of the EAD that is likely to be lost, considering collateral recovery.

iii. Worst-Case Default Ratio:

Reflects the confidence level (e.g., 99.9%) and is derived using Gaussian distributions.

iv. Maturity Adjustment:

Accounts for the loan’s time horizon beyond one year, as longer maturities often increase exposure to risk.

Let’s have a deeper look into the formula. Without going into the exact steps how to derive the formula, we like to show it here and explain the components:

Understanding the Capital Requirement Formula

Without going into the exact steps how to derive the formula, we like to show it here and explain the components.

i. Default Risk and Correlation

The worst-case default ratio is determined using a Gaussian (normal) distribution represented by N in the formula.

It indicates the level of default risk under adverse conditions, influenced by the chosen confidence interval. For instance, at a 99.9% confidence level, institutions prepare for extreme but infrequent losses that might occur once in 1,000 years. The formula includes a correlation factor (rho), which modifies the default ratio based on the probability of default (PD) of an individual loan. Regulators provide predefined formulas for correlations for various asset classes. Below is the formula for corporate and SME loan exposures.

The correlation in this formula depends on the PD, decreasing as PD increases. This is based on the idea that higher PD from idiosyncratic reasons reduces correlation.

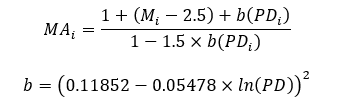

ii. Maturity and Basel Adjustments

The regulatory framework also provides the Maturity Adjustment formula:

The formulas in the regulatory framework included a scaling factor that increased the resulting capital requirement by a defined percentage to account for unconsidered aspects. This scaling factor is being eliminated under the Basel 4 updates.

Practical Example of Quantifying Capital Requirements

Using the Foundation IRB methodology, we apply the formulas to calculate the capital requirements for a hypothetical loan. We will use the loan data from the previous examples:

- Loan amount: $10,000

- PD: 5%

- LGD: 40%

- EAD: 50% of the loan amount (based on mid-term default assumptions).

- Maturity: 4 years

- Confidence level: 99.9%

Step 1: Calculate EL

The EL is determined as follows:

EL = 10, 000 × 5% × 40% × 50% = 100

Step 2: Calculate UL

Step 3: Total Capital Requirements

Total Capital = EL + UL = 100 + 966.49 = 1066.49

Here, $100 is covered by reserves, while $966.49 must be held as equity capital to meet regulatory requirements at the specified confidence level.

Key Observations on Capital Quantification

Understanding the nuances of Unexpected Loss (UL) calculations provides significant insights into risk management. Here are some key observations:

i. Detailed Risk Sensitivity

The UL calculation for each loan accounts for its unique risk profile. This granularity helps institutions precisely set prices and allocate provisions, ensuring that riskier loans are appropriately compensated, and safer loans are competitively priced.

ii. Correlation and Regional Risk Considerations

When loans in a portfolio share exposure to similar external factors, such as a regional economic downturn, the risk of correlated defaults increases. While basic UL formulas, like those in the Foundation IRB approach, do not explicitly account for these correlations, they are crucial for understanding portfolio-level risks. Advanced IRB models or internal methodologies often address this aspect more comprehensively.

iii. Influence of Confidence Levels

Higher confidence levels require significantly more capital to cover extreme loss scenarios. This increase is not linear, as losses in the tail of the distribution have a disproportionately large impact. Institutions must carefully balance the need for regulatory compliance with operational cost-efficiency, particularly in competitive lending markets where high capital requirements may reduce profitability.

Applications of UL Models

The formula for calculating UL is straightforward enough to be implemented using common tools like Excel. This makes it accessible for financial institutions with limited technical resources. However, for more complex scenarios, institutions may need advanced tools and techniques. These include:

- Managing large and diverse portfolios with varied loan types, borrower profiles, and collateral structures.

- Conducting stress tests and analyzing the impact of macroeconomic shocks, such as recessions or market volatility.

- Meeting the demands of highly regulated environments that require detailed reporting and compliance with stringent regulatory standards.

The ability to scale the sophistication of models provides flexibility to financial institutions, allowing them to adapt methodologies to the complexity of their portfolios.

Known Limitations

Although the current methodology provides a solid foundation for calculating UL, it is based on certain assumptions that may not fully align with real-world scenarios:

i. Normal Distribution Assumption:

UL models often assume that losses follow a Gaussian (normal) distribution. However, actual loss patterns, particularly during crises, tend to have “fat tails,” meaning extreme losses are more common than predicted by normal distribution models.

ii. Need for Tailored Models:

Institutions may need to develop customized models to account for specific portfolio characteristics, such as regional risks, unique borrower profiles, or non-standard collateral.

iii. Stress Testing and Scenario Analysis:

Complementary methods, like stress testing and scenario analysis, can enhance the robustness of risk management by simulating extreme conditions beyond standard calculations.

Linking Capital Requirements to Pricing and RAROC Strategies

As a credit risk expert, quantifying capital requirements at the loan level is a strategic tool. The quantification helps you to see the real cost of risk, price loans more accurately, and steer your institution’s portfolio with confidence.

In the next chapter, we will show how you can take these capital figures and apply them directly to pricing and Risk-Adjusted Return on Capital (RAROC), turning risk data into decisions that drive stronger financial outcomes.