The Eight Critical Data Domains for SME Lenders begin with a simple truth: Every SME loan creates proprietary information. Not just financial statements and contracts, but insight: how a business really operates, how it reacts under stress, how management behaves, and how risk evolves over time.

The question is not whether this information exists. It does. The real question is whether the institution learns from it, or loses it.

In the first article of this series, we argued that most SME lenders do not suffer from a lack of data, but from unusable data. Information is fragmented, inconsistent, and poorly structured, undermining decision quality and trust.

In this article, we address the next critical step:

Defining the core data domains that every serious SME lender must deliberately own.

Because without a clear data model, no architecture, governance framework, or AI initiative will ever work.

Data Domains Matter More Than Systems

One of the most common mistakes in SME lending transformation is starting with systems. Core banking. CRM. Credit workflow. Document management. Each is discussed in isolation, often replaced or upgraded independently.

However, systems come and go. Data logic must endure.

If an institution has not defined:

What information it considers critical

How that information is structured

Who owns it

How it connects across the lending lifecycle

Then, any system, old or new, will eventually recreate the same fragmentation. Data domains provide the conceptual backbone of SME lending intelligence. They define what matters, independent of technology choices.

Institutions that define their data domains early:

Build institutional memory

Shorten learning curves

Create a compounding competitive advantage

Those that postpone this decision pay for it repeatedly, in rework, inconsistency, and lost insight.

Quantitative and Qualitative Data: Two Sides of the Same Coin

Before we look at the domains themselves, one principle must be clear:

Good SME lending requires both quantitative and qualitative data.

Financial ratios, repayment histories, and exposure numbers tell one part of the story, and relationship manager observations, site visit notes, and client interactions, tell another.

Most institutions are reasonably good at collecting numbers, even if inconsistently. They are far worse at capturing, structuring, and reusing context.

That context is not “soft data.” It is often the earliest and most accurate indicator of risk or opportunity. A data domain model that ignores qualitative information is incomplete by design.

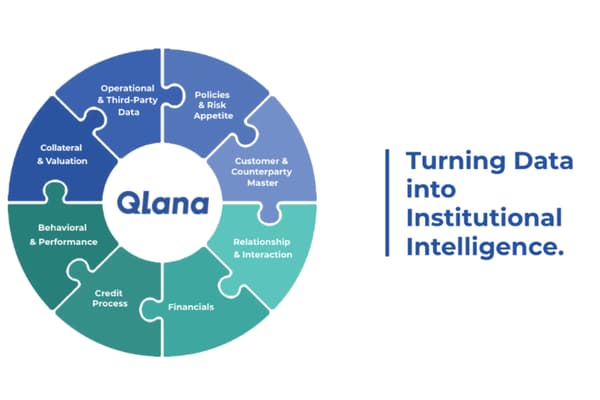

The Eight Critical Data Domains of SME Lenders

Based on extensive work with banks, funds, and financial institutions across markets, eight domains consistently form the minimum backbone of a serious SME lending operation.

They are not theoretical, but practical, battle-tested, and mutually reinforcing.

Part 1 of the Eight Critical Data Domains

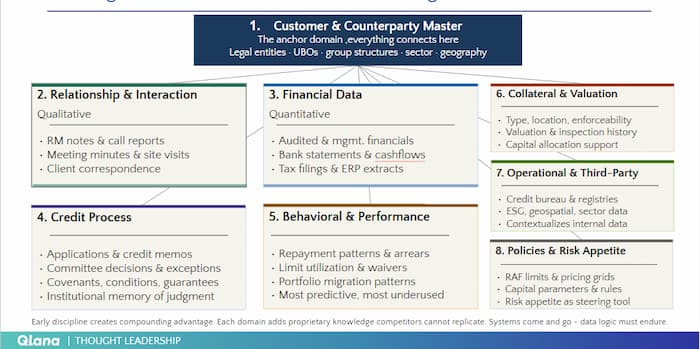

1. Customer & Counterparty Master

This is the anchor domain. Everything else connects here.

It includes:

Legal entity data

Ownership and ultimate beneficial owners (UBOs)

Group structures and related parties

Sector classification (ISIC or equivalent)

Geographic footprint

Without a clean customer master:

Duplicates proliferate

Group exposures remain hidden

Concentration risk becomes invisible

This domain establishes unique identifiers and data lineage. If this is weak, everything built on top of it is unstable.

2. Relationship & Interaction Data

This domain captures the human side of SME banking.

It includes:

RM call reports

Meeting minutes

Site visit notes

Client correspondence

Internal assessments and observations

This is where most institutions lose critical knowledge. When relationship insight lives only in inboxes or free text, it disappears when people leave or portfolios change. Structured interaction data turns individual experience into institutional intelligence.

Over time, this domain becomes a powerful early-warning and opportunity-detection layer.

3. Financial Data

This is the quantitative backbone of credit assessment.

It includes:

Audited and management financial statements

Projections and budgets

Bank statements and cash flow data

Tax filings or ERP extracts

The challenge here is not availability, it is consistency over time. Well-managed financial data allows:

Trend analysis

Automated ratio calculation

Comparability across clients and segments

Poorly managed financial data forces analysts to start from zero with every review.

4. Credit Process Data

This domain documents how decisions are made.

It includes:

Credit applications

Credit analyses and memos

Committee decisions

Covenants, conditions, and guarantees

Approval rationales and exceptions

This is the institutional memory of credit judgment.

Without structured credit process data:

Decisions cannot be reproduced

Exceptions cannot be analyzed

Learning is lost

Strong institutions treat this domain as a strategic asset, not a compliance artifact.

Part 2 of the Eight Critical Data Domains

5. Behavioral & Performance Data

This domain captures what actually happens after approval.

It includes:

Repayment behavior

Arrears and restructurings

Limit utilization

Waivers and breaches

Portfolio migration patterns

Behavioral data is often the most predictive, and the most underused.

Over time, this domain feeds:

Early warning systems

PD calibration

Differentiated pricing

Proactive portfolio management

Ignoring behavioral data means repeating the same mistakes.

6. Collateral & Valuation Data

Collateral is not just a legal appendix.

This domain includes:

Collateral type and characteristics

Location and enforceability

Valuation and revaluation history

Inspection and monitoring records

Poor collateral data leads to:

Overestimated recovery values

Weak provisioning

Surprises during enforcement

Structured collateral data supports both risk management and capital allocation.

7. Operational & Third-Party Data

This domain enriches internal views with external context.

It includes:

Credit bureau information

Business registries

ESG self-assessments

Geospatial or sector data

Trade or invoice-level data (where relevant)

External data does not replace internal knowledge. It contextualizes it.

Institutions that integrate third-party data intelligently see patterns earlier and price risk more accurately.

8. Policies & Risk Appetite Data

This domain defines the boundaries of acceptable risk.

It includes:

Risk appetite limits

Sector and obligor thresholds

Pricing grids

Capital allocation parameters

Policy rules and exceptions

When this domain is not explicitly linked to exposures and decisions, risk appetite becomes theoretical. When it is integrated, it becomes a steering mechanism.

Early Discipline Creates a Compounding Advantage

Many institutions postpone formal data domain design until their SME portfolio has reached scale. That is a mistake.

Early discipline means:

Cleaner data from day one

Faster learning cycles

Fewer legacy issues

Easier automation later

Each loan, interaction, and decision adds to a growing proprietary knowledge base that competitors cannot easily replicate. This compounding effect is one of the most underappreciated advantages in SME lending.

Data Domains Are Leadership Decisions

Defining data domains is not a technical exercise. It requires:

Strategic clarity

Business ownership

Leadership commitment

Someone must decide:

What data matters

Who owns it

How it will be used

Without that clarity, even the best systems degrade over time.

Strong SME lenders understand this:

data structure reflects management discipline.

About This Series

This article is part of Q-Lana’s four part Data Management series on how modern SME lenders turn fragmented information into decision intelligence.

The complete framework, includes the articles on

- Concepts of good data management,

- The eight critical data domains,

- Minimum viable data architecture, and

- Data governance, quality, and knowledge management,

The full content in a more detailed version is available in Q-Lana’s Data & Knowledge Management Whitepaper.