Most SME lending data initiatives fail for a predictable reason. They try to build the perfect architecture before delivering any value.

Enterprise data lakes

Complex integration layers

Multi-year IT roadmaps

Dozens of dashboards, but only a few of them trusted

After months (or years), the business still asks the same question: Can we make faster, better credit decisions?

Too often, the honest answer is no. The problem is not ambition. The problem is sequence.

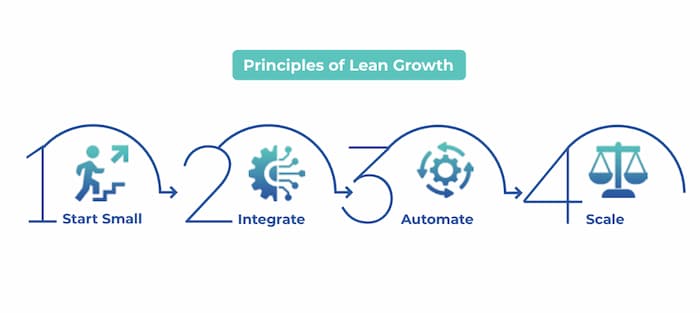

In SME lending, data architecture must enable decisions now, not promise insight later. That is why the most effective institutions don’t start with a “target architecture.” They start with a minimum viable data architecture, designed to work with what already exists, prove value quickly, and scale with discipline.

Why Big Data Architectures Fail in SME Lending

Large-scale data programs often fail not because they are technically flawed, but because they misunderstand how SME lending actually works.

Typical failure patterns include:

Perfection paralysis: Projects stall while teams debate future use cases instead of fixing today’s problems

Over-engineering: Sophisticated architectures are built before data quality, ownership, or definitions are resolved

Low adoption: Business users don’t trust the outputs and revert to spreadsheets and emails

Delayed credibility: By the time results appear, priorities and people have changed

SME lending is not a laboratory environment. It is fast, judgment-driven, and operationally intense. A data architecture that does not deliver early, visible value will lose support, regardless of how elegant it looks on paper.

What is Minimum Viable?

“Minimum viable” does not mean simplistic or temporary.

It means:

Lean rather than bloated

Connected rather than fragmented

Controlled rather than ad hoc

A minimum viable data architecture (MVDA) focuses on enabling the next best decision, not the perfect future state. Its purpose is to answer four practical questions, reliably and repeatedly:

Do we have all relevant information for this decision?

Is it consistent and trusted?

Can we trace how the decision was made?

Can we reuse this information next time?

If an architecture supports these questions, it is doing its job.

The Six Building Blocks of a Minimum Viable Data Architecture

Across institutions and markets, six architectural components consistently form the backbone of an effective SME lending data setup. They are modular, technology-agnostic, and designed to evolve.

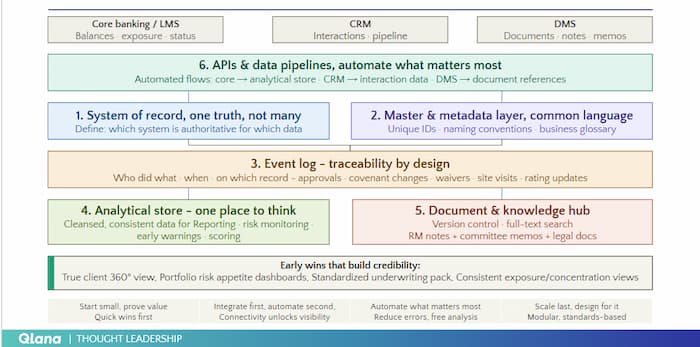

1. System of Record – One Truth, Not Many

Every institution already has systems that matter:

Core banking or loan management

CRM

Accounting systems

The problem is not their existence, it is ambiguity. A minimum viable architecture clearly defines which system is authoritative for which data:

Customer identity

Facility balances

Repayment status

Exposure amounts

Without this clarity, reconciliation becomes a permanent activity, and trust erodes.

You do not need fewer systems. You need clear authority.

2. Master & Metadata Layer – Common Language, Shared Meaning

Data without definition is noise.

This layer establishes:

Unique identifiers for customers, facilities, and collateral

Standard naming conventions

A business glossary that defines fields and metrics

This is not academic documentation. It is what allows different teams, credit, risk, finance, audit, to speak the same language.

Institutions often underestimate this step. In reality, it is one of the highest-return investments in data work.

3. Event Log – Traceability by Design

Every meaningful action in SME lending matters:

Credit approvals

Covenant changes

Waivers

Site visits

Rating updates

A structured event log records:

Who did what

When it happened

On which data object

This creates decision lineage, the ability to reconstruct not just outcomes, but reasoning.

Event logs are the foundation of:

Audit readiness

Model validation

Explainable AI

Institutional learning

Without them, institutions rely on memory and email trails. That does not scale.

4. Analytical Store – One Place to Think

This is where trusted, cleansed data comes together for:

Reporting

Portfolio analysis

Risk monitoring

Early warning systems

Whether implemented as a warehouse or lakehouse is secondary. What matters is that:

Data is consistent

Refreshed predictably

Separated from operational noise

This store is not for experimentation alone.

It is for decision support.

5. Document & Knowledge Hub – Where Context Lives

SME lending is document-heavy:

Financial statements

Credit memos

RM notes

Committee minutes

Legal documentation

A minimum viable architecture consolidates these into a single document and knowledge hub with:

Strict version control

Searchable content

Links to structured data

This is where qualitative insight meets quantitative facts.

Institutions that neglect this layer lose the “why” behind decisions, even if they retain the “what.”

6. APIs & Data Pipelines – Automate What Matters

Manual file transfers are a hidden tax on SME lending.

Automated pipelines:

Reduce errors

Improve timeliness

Free up analytical capacity

A minimum viable setup focuses on high-impact flows first:

Core systems → analytical store

CRM → interaction data

DMS → document references

Automation follows clarity, not the other way around.

Early Wins That Build Credibility

The purpose of a minimum viable architecture is to show value early. Typical early outputs include:

A true Client-360 view

Portfolio risk appetite dashboards

Standardized underwriting packs

Consistent exposure and concentration views

These do not require perfection. They require consistency. Once users see reliable outputs, trust builds, and adoption follows.

Architecture Does Not Replace Governance

A common misconception is that architecture enforces discipline. It does not.

Architecture enables discipline. Governance enforces it. Without clear ownership, data quality rules, and follow-up mechanisms, even the best architecture will decay over time. This is why architecture and governance must evolve together, a topic we will address explicitly in the next article.

Why This Approach Works for SME Lending

The minimum viable approach succeeds because it aligns with reality:

SME portfolios grow incrementally

Credit judgment evolves over time

Resources are finite

Trust must be earned, not declared

Institutions that adopt this approach move faster not because they do less, but because they do the right things first.

Institutions that adopt this approach move faster not because they do less, but because they do the right things first.

At Q-Lana, this philosophy is embedded into how we design platforms and implementation journeys. We focus on:

Early decision impact

Pragmatic sequencing

Architectures that serve the business – not the other way around

About This Series

This article is part of Q-Lana’s four part Data Management series on how modern SME lenders turn fragmented information into decision intelligence.

The complete framework, includes the articles on

- Concepts of good data management,

- The eight critical data domains,

- Minimum viable data architecture, and

- Data governance, quality, and knowledge management,

The full content in a more detailed version is available in Q-Lana’s Data & Knowledge Management Whitepaper.