One of the most persistent objections to customer-centric lending is also one of the most seductive: “Every SME client is different.”

It is true, up to a point. Ownership structures differ. Sectors differ. Management teams bring different instincts and track records. But spend long enough talking to SME clients across industries and geographies, and a different pattern emerges. The problems they face are far less unique than most banks’ internal processes would suggest. Cash-flow gaps, working-capital pressure, FX exposure on thin margins, growth that outpaces available liquidity, these recur constantly. The names and industries change. The underlying mechanics rarely do.

The mistake is not in acknowledging that clients differ. The mistake is in treating every instance of a familiar problem as if it were a genuinely novel situation. That impulse, well-intentioned, often defended as prudence, is what makes SME lending slow, inconsistent, and harder to manage at scale than it needs to be.

Why “Every Case Is Different” Is a Risky Mindset

In traditional lending models, each transaction is treated as a bespoke exercise. Credit memos are rewritten. Structures are debated from the beginning. Risk discussions start at zero, even when the underlying situation closely resembles cases the bank has handled dozens of times before.

As a result, this has three consequences:

Speed suffers

Every new deal requires full re-analysis, even when the underlying problem is familiar.Consistency erodes

Similar clients receive different structures depending on who handles the case.Learning is lost

Successful (and failed) solutions are not systematically reused.

What makes this particularly difficult to address is that the bespoke approach feels rigorous. It signals care and attention. In reality, it creates hidden risk: decisions become harder to compare, policy drift goes undetected, and exceptions quietly become the norm. Customer centricity cannot scale under those conditions. It requires something more disciplined: the ability to recognize patterns and respond to them consistently.

Problem Archetypes: Making Client Needs Comparable

The foundation of a scalable customer-centric model is a shared vocabulary for describing client problems. Problem Archetypes are standardized representations of recurring client situations. Each archetype describes the underlying business challenge, the typical financial symptoms it produces, the key risk drivers to monitor, and the outcome a good solution must achieve.

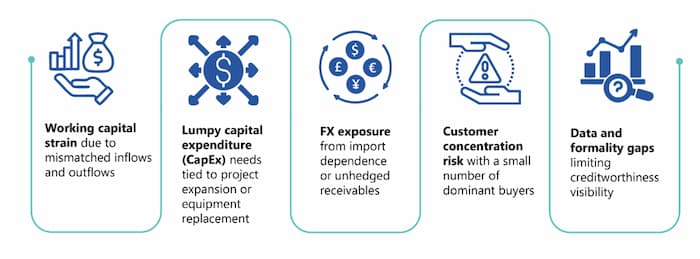

The examples are familiar to anyone who has spent time in SME banking: seasonal cash-flow volatility in trading businesses, working-capital strain driven by long receivable cycles, FX exposure where export revenues arrive in a currency that does not match the cost base, growth financing where leverage limits become the binding constraint. These are not exotic situations. They are the everyday reality of SME finance.

Examples include:

Importantly, these archetypes are not products. They are diagnostic categories. Their purpose is to make client situations comparable across portfolios and across teams. Relationship managers, credit officers, and risk colleagues can discuss a client situation with a shared frame of reference instead of each starting from their own interpretation. And decisions can be made faster, because the diagnosis is already half the work.

From Archetypes to Solution Toolkits

Problem Archetypes only create value when they are linked to what happens next. A Solution Toolkit is a pre-approved combination of instruments, structures, and controls designed to address a specific archetype, one that has already been validated against the bank’s Risk Appetite Framework (RAF).

A toolkit typically defines:

Eligible products and structures

Target maturities and amortization profiles

Collateral expectations

Covenants and monitoring triggers

Pricing corridors

Escalation thresholds

The shift this creates is more significant than it might appear. Instead of asking “What can we approve for this client?” the team asks “Which approved solution fits this problem, and under what conditions?” That is not a subtle reframing. It changes where the work starts, how fast decisions move, and how consistently they land

Risk Appetite Moves Upstream

In many banks, risk appetite enters the lending process late. A structure is proposed, debated, sometimes partially agreed upon, and only then checked against sector limits, concentration rules, and capital allocation logic. This sequencing is inefficient, and it sets up an adversarial dynamic between origination and risk functions that neither side particularly enjoys.

Solution Toolkits reverse the sequence. Each toolkit is designed from the outset to sit within defined risk parameters: sector limits, leverage thresholds, concentration rules, capital allocation logic. Risk appetite is not applied after the fact. It is embedded in the solution architecture from the beginning.

This changes the role of the risk function from gatekeeper to co-designer, and it changes the tenor of internal discussions from approval versus rejection to how to solve the problem safely. Customer centricity without that discipline would quickly erode portfolio quality. With it, the model becomes something different: a risk-aware growth engine rather than a compliance exercise.

Speed Without Loss of Judgment

The most common objection to this kind of framework is that it reduces skilled professionals to process-followers. That concern is understandable, but it misunderstands what Solution Toolkits actually do.

A toolkit does not tell a relationship manager how to handle a client. It answers the routine questions in advance:

Is this type of solution acceptable?

Under which conditions?

With which safeguards?

Once those questions are settled, the judgment that actually matters can come to the surface.:

Is the client correctly diagnosed?

Do they truly fit the archetype?

Are there specific risks that require adaptation?

Is an exception justified, and why?

In other words, judgment is no longer spent on reinventing the basics. Instead, it is applied where it adds real value.

Learning Becomes Institutional

One of the quieter benefits of Problem Archetypes and Solution Toolkits is what they make possible over time. When problems and solutions are structured consistently, outcomes become comparable. Performance can be tracked by archetype rather than just by borrower. Early warning signals can be refined based on observed patterns rather than anecdote. The bank can begin to answer questions it could never previously ask with confidence: Which archetypes perform best across the cycle? Which structures reduce volatility most effectively? Where do exceptions pay off, and where do they consistently underperform?

Banks that continue to treat every case as sui generis never reach this stage. They remain dependent on the memory of individual bankers and the informal transmission of tacit knowledge, both of which leave with people when they move on. Structured problem-solving turns that knowledge into institutional capital.

The Role of Data and AI – Assistance, Not Autonomy

Problem Archetypes and Solution Toolkits are naturally data-friendly. Behavioral signals and financial ratios can help identify likely archetypes early, confirm or challenge relationship manager intuition, and monitor whether solutions are performing as intended over time.

AI can contribute meaningfully: flagging probable archetypes based on observed patterns, checking toolkit eligibility and policy compliance, monitoring for deviations and emerging risk concentrations. But the role of AI here is assistive, not autonomous. The methodology comes first. AI improves consistency and speed once that foundation is in place. It does not replace the judgment required to diagnose a client situation or decide whether an exception is warranted.

AI assists. Humans decide.

This is not a limitation to be overcome. It is a deliberate design choice. The value of these tools comes precisely from the fact that humans remain accountable for decisions, with AI supporting them rather than substituting for them.

Why This Matters More Than Ever

Volatile markets expose the cost of improvisation. When stress increases, ad-hoc decisions multiply, exceptions accumulate, and portfolios lose coherence. Banks that rely on bespoke judgment across the board find it difficult to respond consistently because there is no shared frame of reference to anchor decisions when pressure is high.

Banks that have defined their problem archetypes, pre-approved their solution toolkits, and embedded their risk appetite into the architecture of lending decisions are in a different position. They can move quickly without losing control, because the boundaries are already set. Customer centricity, structured this way, becomes a stabilizing force rather than a source of additional variability

From Philosophy to Execution

This article marks a turning point in the series. We move from intent to execution. Customer centricity is no longer:

A mindset

Or an operating aspiration

It becomes:

A decision architecture

A risk-aligned playbook

A platform for learning

In the next article, we will zoom in on the moment of truth: the client conversation itself, and how a structured discovery script turns dialogue into diagnosis.

Closing Thought

Customer centricity does not mean starting from scratch every time. It means recognizing patterns, applying discipline, and using judgment where it matters most. That is how banks move from improvisation to engineered problem solving in SME lending.

Setting the Stage for the Series

This article is part of Q-Lana’s six part Customer centricity on how modern SME lenders turn fragmented information into decision intelligence.

The complete framework, includes the articles on:

The full content in a more detailed version is available in Q-Lana’s Customer Centricity in SME and Corporate Lending Whitepaper.