Real customer centricity starts with a simple shift: From selling products to solving client business problems, within a clear risk framework. The key question is no longer: “Which product fits this client?”, but rather, “which problem is the client trying to solve, and how can we support that safely?” – We made the case that the implementation of a customer centric business model is timely and addresses both, the needs of SMEs to get funding, as well as the banks to deliver value to their customers that is truly differentiable.

Of course, its quite easy to convince a bank’s senior management of the benefits, and yet still customer centricity projects fail. Not because of a disagreement with the idea, but rather because banks try to deliver it through operating models that were never designed for it.

Most lending organizations are built around silos: front office, credit, risk, products, operations. That structure optimizes internal control. It does not optimize client outcomes. From a client’s perspective, these silos are invisible. From a bank’s perspective, they create friction, delay, and fragmented solutions.

From a client’s perspective, these silos are invisible. From a bank’s perspective, they create friction, delays, and fragmented solutions. If customer centricity is meant to move lending from product selling to problem solving, then the operating model must change accordingly. Not radically. Not expensively. But deliberately.

Why Silo-Based Lending Breaks Customer Centricity

In a silo-based model, customer outcomes are accidental. A relationship manager identifies a client need. Credit evaluates risk.

Products are selected based on availability. Operations execute what was approved.

At no point is there a single, shared view of:

The client’s underlying problem

The desired business outcome

How different functions contribute to solving it safely

The consequences are familiar:

Long turnaround times

Repeated back-and-forth between teams

Inconsistent structuring

Frustrated clients who feel they are “re-explaining” their business at every step

From a risk perspective, this fragmentation is dangerous. Information is lost at handovers. Judgment is diluted. Responsibility is diffused. Customer centricity cannot thrive in this environment, no matter how good the intentions.

The False Choice: Reorganization or Status Quo

When banks recognize these issues, they often assume there are only two options:

Keep the current structure and accept its limits

Launch a major reorganization

Both are flawed. Large-scale reorganizations are disruptive, politically sensitive, slow to deliver results and often reversed within a few years. At the same time, keeping the status quo guarantees that customer centricity remains a slogan. The solution lies in a third path: changing how work gets done, not how the organization chart looks.

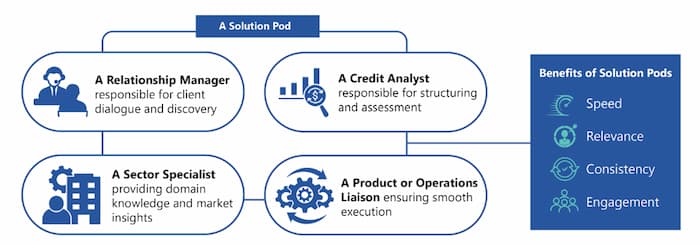

Introducing Solution Pods: Collaboration Without Chaos

Solution Pods are cross-functional working units that come together around a specific client problem, not around a product or department. They do not replace existing teams. They overlay them.

A typical Solution Pod may include:

A Relationship Manager

A Credit Analyst

A Risk representative

Where relevant, product or treasury expertise

What changes is not reporting lines, but focus. Instead of each function optimizing its own step, the Pod aligns around:

A shared understanding of the client problem

A clear target outcome

Predefined risk boundaries

This sounds modest, but its effects are not. Decisions accelerate because the relevant expertise is in the room together rather than communicating through layers. Rework declines because misunderstandings are surfaced earlier. Accountability becomes clearer because the team has a shared definition of what success looks like. Customer centricity moves from being a stated intention to something that is actually organized for..

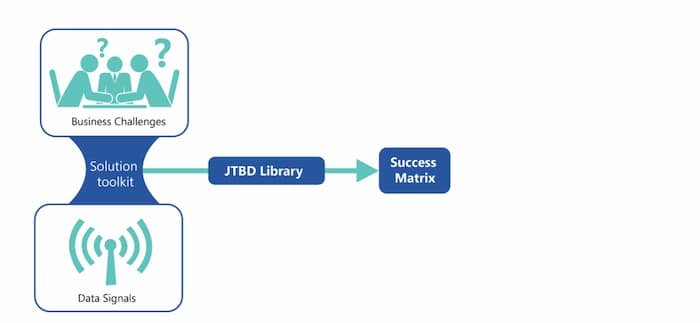

Jobs-to-Be-Done: A Shared Language for Problem Solving

Solution Pods only work if teams share a common language. That language is provided by Jobs-to-Be-Done (JTBD).

In practice, this means moving from “the client wants a term loan” to “the client needs to smooth seasonal cash-flow volatility without increasing balance-sheet leverage.” The difference is not semantic. The product framing closes down the conversation. The problem framing opens it up and invites a diagnostic response rather than a transactional one.

A standardized library of Jobs-to-Be-Done statements, built around the recurring structured problem statements. They can be developed and expanded over time, by sector, company size, or other dimensions. A JTBD library structures RM conversations, gives Credit and Risk comparable cases, and makes solutions reusable and scalable. JTBD becomes your solutions knowledge base. JTBD creates a bridge between empathy and discipline.

From Hero RMs to Institutional Capability

In many banks, customer centricity depends on exceptional individuals. Experienced RMs know whom to call, how to navigate processes, and how to compensate for system gaps. They are the institution’s rainmakers.

They are essential, but because this expertise develops slowly over decades, it is not easily scalable. The result is inconsistency, dependence on individuals, and knowledge loss when people move.

Solution Pods and JTBD translate customer centricity from individual heroics into institutional methodology. Judgment is not constrained; it is supported by structure.

The Role of the RM Copilot: Making Collaboration Simple

Even well-designed operating models fail if they are too cumbersome to use consistently. This is where intelligent workflow support becomes valuable. An RM Copilot, not a decision-maker, but a workflow intelligence layer, can prepare client diagnostics, structure problem statements in a consistent format, assemble relevant data automatically, and guide the process within defined risk appetite boundaries.

For the relationship manager, this means less time on manual preparation and more time with clients. For credit and risk, it means better-prepared cases arriving with consistent framing and transparent logic. The Copilot does not replace the collaboration that happens within a Solution Pod. It reduces the friction that would otherwise make that collaboration too expensive to sustain.

Customer Centricity and Risk Appetite: Designed Together

A key advantage of this model is that risk appetite is present from the start. Instead of proposing solutions first and checking policy later, Solution Pods operate inside predefined risk corridors. Sector limits, leverage thresholds, and concentration rules are considered early.

This prevents teams from building cases that end in binary approval-versus-rejection outcomes at committee level. The goal is joint problem-solving within constraints. Risk becomes a steering mechanism, not a brake.

Why This Operating Model Improves Speed and Quality

Banks that adopt this model typically find that turnaround times fall, iterations between teams decrease, and structuring becomes more consistent across comparable situations. But the more significant benefit accrues over time. When problems are framed consistently and solutions are tracked against outcomes, patterns emerge that would otherwise remain invisible. Which structures perform best? Which client situations tend to deteriorate, and at what stage? Where do exceptions add value, and where do they quietly erode portfolio quality? These are questions a silo-based model can never reliably answer. A Pod-based model begins to answer them systematically

Minimal Change, Maximum Impact

One of the most important characteristics of this operating model is its pragmatism. It does not require:

A new org chart

Massive IT projects

Wholesale cultural transformation

It requires:

Clear problem definitions

Structured collaboration

Disciplined execution

This makes it implementable in real institutions, not just in theory.

Setting the Stage for the Next Step

This article has focused on the operating model: how banks can move from silo-based execution to collaborative problem-solving through Solution Pods, JTBD, and RM support tools.

In the next article, we will go one level deeper: how recurring client problems can be translated into standardized, risk-approved solution toolkits, without losing flexibility or judgment.

Closing Thought

Customer centricity does not scale through goodwill. It scales through designed collaboration. Banks that understand this do not need to reorganize every few years. They need to change how work actually happens , and then protect that change with structure and discipline.

Setting the Stage for the Series

This article is part of Q-Lana’s six part Customer centricity on how modern SME lenders turn fragmented information into decision intelligence.

The complete framework, includes the articles on:

The full content in a more detailed version is available in Q-Lana’s Customer Centricity in SME and Corporate Lending Whitepaper