The Illusion of High Risk

Many institutions still assess SME credit risk with tools originally designed for corporates. Financial statements are reviewed backward-looking, ratio thresholds are applied rigidly, and collateral often becomes the dominant comfort factor. Approval processes are frequently detached from how SMEs actually generate cash.

Meanwhile, many SMEs operate with informal or semi-formal records. They combine household and business cash flows. They demonstrate strong sector logic and resilience but lack balance-sheet polish. What banks often see as opacity is, in reality, a difference in structure.

The predictable outcome is caution. And caution is not wrong. But without structured capability, caution becomes over-collateralization, missed opportunities, and inconsistent decisions.

The issue is not prudence. The issue is the ability to create decision-quality with imperfect information.

Want to benchmark your SME credit capability?

Existing Approaches Fall Short: That’s Good News

Over the years, many institutions have invested in SME training. Staff attend international virtual courses. They work on global case studies. They return well informed. But often, they are not empowered.

Why? Because the training rarely changes how credit decisions are made on Monday morning. It does not integrate with the institution’s workflows. It does not connect analysis, structuring, monitoring, and governance into one coherent discipline. This is not a failure of effort. It is a design limitation.

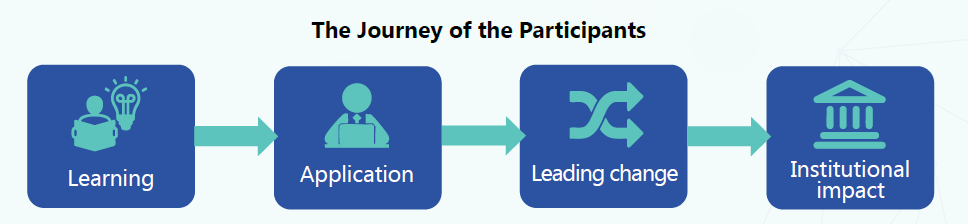

And that is precisely the opportunity. The next generation of SME finance training programs must move from knowledge transfer to capability formation. From theory to applied discipline. From generic cases to real local SMEs.

SME Finance Is an Engineered Discipline

Effective SME lending is engineered, not improvised. It requires institutions to master a connected chain of capabilities: understanding how SMEs operate, reconstructing reliable cash flows, structuring facilities aligned with risk appetite, and monitoring proactively before warning signs become arrears.

Break any link in that chain, and portfolio quality suffers, often quietly at first.

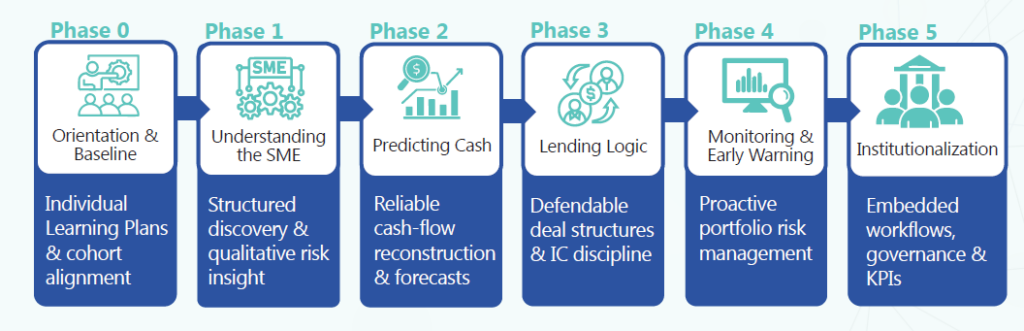

This is the insight behind the SME Finance Excellence Program. It is designed as a six-month institution-building journey, not a classroom event. Participants work on real SME cases in their own market. They produce the same artifacts required in daily credit work: cash-flow forecasts, risk maps, term sheets, monitoring dashboards, early-warning triggers, and committee-ready decision notes.

By the end, institutions do not simply have trained staff. They have strengthened routines, shared language between business and risk, and practical tools embedded in their operations.

Why Localization Matters

SME finance cannot be imported as a template. Cash cycles in agriculture differ from trade. Informality varies by country. Regulatory constraints differ across regions. Sector exposure patterns are local. Even behavioral norms in credit committees are local.

That is why we are building partnerships to localize the program across markets. Banking associations, MFI associations, financial groups, and development platforms can host and co-brand the program. Trainers are selected locally. Cases are drawn from local sectors. Participants work on local SMEs.

Q-Lana provides the methodology, supervision, quality standards, and learning architecture. The market provides the context. Together, this creates something powerful: global discipline with local relevance.

A Stronger Future for SME Finance

The demand for SME finance is not the problem. The ambition is not the problem. The liquidity, in many cases, is not even the problem.

The opportunity lies in professionalizing SME lending so that growth and risk management move together.

Institutions that invest in structured capability typically see stronger portfolio quality, clearer risk appetite alignment, and more confident expansion into underserved segments. They build trust with SMEs not by relaxing standards, but by applying them intelligently.

This is an optimistic story. SME lending does not need to be scaled recklessly. It needs to be structured deliberately. And when capability improves, performance follows.

Introducing the SME Finance Excellence Program

SME finance is not held back by a lack of ambition. It is held back by a lack of repeatable capability. the ability to make high-quality credit decisions, monitor proactively, and act early, consistently, across teams and branches.

Christian Ruehmer (Co-Founder & CEO)

To address this, we designed the SME Finance Excellence Program, a six-month institution-building journey, not just an online or classroom event.

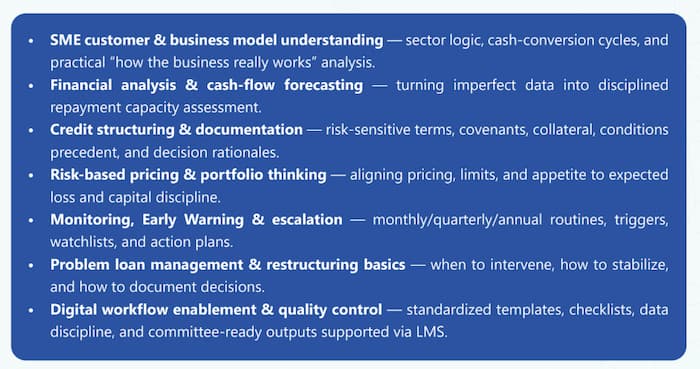

Key Components of the Program

What This Program Does Differently

The program is built around one non-negotiable principle: If learning does not change how credit decisions are made, it has failed. Participants work on real SME cases and build practical institutional assets using:

Structured discovery scripts – don’t stop until you really understand the SME

Cash-flow reconstruction models – it’s cash, not profit, that pays the debt service

Risk hypothesis frameworks – identify the key risks to focus on and mitigate them

Term-sheet logic tied to risk appetite – you can reduce the risk through active risk management

Monitoring dashboards and early-warning indicators – allowing for interventions when the covenant headroom shrinks

Each module produces usable outputs, not just knowledge. By the end, institutions don’t just have trained staff, they have an SME Lending Playbook embedded into their operations.

Moving Forward

If you are a financial institution seeking to strengthen SME lending discipline, we would welcome a conversation about running an in-house cohort.

If you are a banking association, MFI network, or industry platform looking to strengthen the SME finance ecosystem in your country or region, we are actively seeking partners to localize and embed the SME Finance Excellence Program in your market.

SME finance is not failing because SMEs are too risky.

It is underperforming because institutions have not yet fully engineered the capability to manage that risk at scale.

Fix the capability, and the portfolio follows.

Partner With Us

If you are a banking association, development partner, or industry body, we can structure a partnership around:

Member value proposition + certification pathway

Regional cohorts and sponsorship models

Institutional diagnostics + baseline capability assessment

Ready to explore a partnership?