What Capital Is Actually For

Provisions cover Expected Loss, what you plan to lose. Capital covers Unexpected Loss, what you cannot predict with certainty.

Once losses exceed Expected Loss, every additional dollar falls on equity. This is where solvency comes under pressure. This is where regulators intervene. This is where lending contracts at the worst possible moment.

Capital is therefore not about compliance. It is about survivability under stress, and about the confidence to keep lending when competitors cannot.

Institutions that allocate capital precisely are able to:

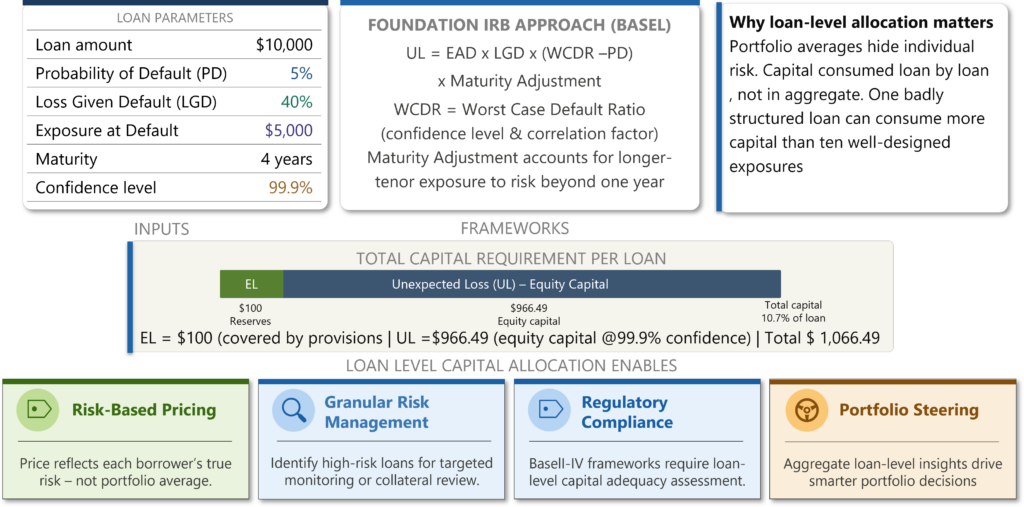

Price risk accurately rather than by intuition or competitive pressure

Compare transactions on a consistent basis, regardless of structure or product type

Steer portfolios proactively, not reactively

Grow without accumulating fragility in the process

What Basel Really Tries to Do

The Basel frameworks are frequently discussed as regulatory overhead. Strip away the complexity and the objective is straightforward: ensure that institutions hold capital in proportion to the risk they actually take.

Basel has evolved not to add bureaucracy, but to correct recurring failures in how risk was measured and capitalized. Its evolution, from the blunt 8% ratio of Basel I through the risk-sensitive internal models of Basel II and III to the recalibrations of Basel IV, reflects a pattern of crises followed by corrections.

At its core, Basel forces institutions to confront a simple question: how much capital does this specific exposure require if things go wrong?

That question is uncomfortable but essential

The Q-Lana White Paper on Credit Risk provides a detailed walkthrough of the Basel frameworks, from the Foundation IRB approach to the output floor under Basel IV, including worked capital calculations for individual loans. For teams responsible for regulatory capital reporting or internal capital adequacy assessments, it is required reading.

▌ The regulatory reality

Basel IV’s output floor, which limits the benefit banks can derive from internal models, is a direct response to institutions using model sophistication to reduce capital below levels that reflect genuine risk. The regulatory direction of travel is clear: capital must reflect risk, not model ingenuity.

Allocating Capital at the Loan Level: Why It Changes Behavior

When capital allocation is visible at the individual transaction level, decisions change. Not because lending standards are imposed from above, but because the economics become transparent.

A loan with a higher PD, weaker collateral, and longer maturity may still be attractive, but only if the return compensates for the capital it consumes. Without that visibility, relationship managers optimize for margin. With it, they optimize for risk-adjusted return. These are very different objectives.

Loan-level capital allocation exposes:

The true cost of risky structures that look attractive on the surface

The capital efficiency of well-secured, shorter-tenor exposures

The hidden cost of concentration, when too many loans share the same risk factors

The genuine pricing floor below which a loan destroys capital rather than creates value

When these dynamics are visible, structuring suddenly matters. Collateral quality becomes economically meaningful. Pricing discussions become factual rather than positional.

“Without loan-level capital visibility, institutions systematically overestimate profitability and underestimate volatility.”

The Non-Linear Cost of Confidence

As confidence levels increase, as institutions choose to hold capital against more extreme loss scenarios, capital requirements grow non-linearly. Moving from a 95% to a 99% confidence level requires additional capital. Moving from 99% to 99.9% requires substantially more.

This is not a technical quirk. It reflects the reality of loss distributions: extreme losses are rare, but severe. Choosing a confidence level is therefore not a calibration exercise. It is a strategic decision about how much volatility the institution can and should absorb, and that decision is inseparable from risk appetite.

An institution that wants to survive almost all scenarios must hold significantly more capital. An institution willing to accept higher volatility can operate with less. Neither is inherently right or wrong. What is dangerous is pretending that these decisions are neutral.

Capital Discipline Improves Lending Quality

When capital allocation is explicit and loan-level, institutions naturally improve the quality of what they originate. Not because they reject more deals, but because the economics drive better structuring.

Capital-aware institutions tend to:

Shorten maturities where possible, reducing capital consumption without reducing yield

Negotiate stronger collateral structures, freeing capital while improving recoveries

Adjust exposure profiles to avoid concentration penalties

Decline transactions that look profitable but quietly destroy capital

This is not risk aversion. It is risk intelligence. The distinction matters enormously for culture and for competitive positioning.

Capital-aware institutions do not stop lending in downturns. They lend selectively and often gain market share while less disciplined competitors’ retreat.

Capital as a Steering Tool, Not a Brake

The most sophisticated institutions use capital allocation to steer the business, not constrain it. They use it to identify under-utilized risk capacity, rebalance sector concentrations, adjust growth targets dynamically, and link strategy to resilience.

Capital becomes the connective tissue between risk measurement, pricing discipline, portfolio management, and strategic ambition. It is where risk management stops being defensive and starts being genuinely useful.

▌ Q-Lana’s approach

Capital allocation is a core element of how Q-Lana builds lending platforms and supports advisory engagements. Every transaction in our platform is assessed not just for credit quality but for its capital consumption and contribution to portfolio-level risk. Capital is not a number reviewed quarterly, it is a variable visible in real time, at the point of decision. This reflects our belief that credit risk management is not a compliance function. It is a competency that should live at the center of an institution’s business model.

▌ Q-Lana Knowledge Resources

White Paper: Credit Risk and Risk Appetite, Part 1 includes worked Basel IRB capital calculations and a detailed treatment of individual loan UL. Download at q-lana.com.

Q-Lana Financial Skills Campus (FSC): Class 1, Credit Risk Measurement and Capital. Covers Basel approaches, capital allocation at the loan level, and the relationship between confidence levels and capital requirements.

FSC Course: Portfolio Management and Capital Optimization, connecting loan-level capital discipline to portfolio-level steering and strategy.

Coming Next

Once capital is allocated at the loan level, a natural question emerges: Are we being paid enough for the capital we put at risk? That question leads directly to RAROC, and Article 4 explains why it is one of the most powerful steering tools available to any lending institution.