What RAROC Actually Measures

At its core, RAROC answers one question: are we being paid enough for the capital we put at risk?

The logic flows directly from the framework established in Articles 1 to 3:

Expected Loss reflects the cost of risk, provisioned and priced in

Unexpected Loss defines how much equity capital must be held against the exposure

Capital is the scarce resource that shareholders expect to be compensated for

RAROC expresses return relative to that capital, not relative to loan size or headline margin

This reframes profitability entirely. A loan with a high interest rate and poor collateral may generate less value than a well-secured loan at a lower rate, because the capital it demands is far greater.

RAROC makes that trade-off explicit, visible, and comparable across every transaction in the portfolio.

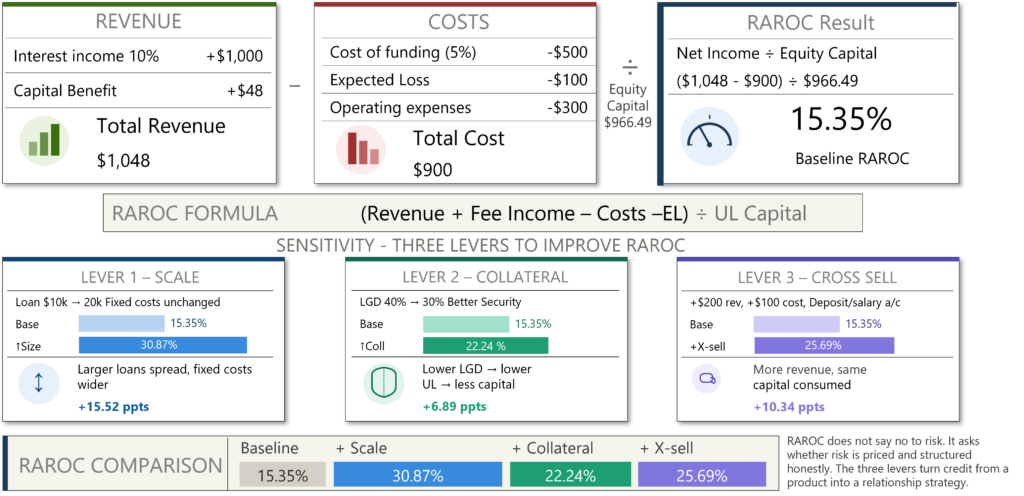

The Q-Lana White Paper on Credit Risk includes a full worked RAROC calculation, including sensitivity analysis across loan size, collateral quality, and cross-selling scenarios, for teams that want to see the full mechanics before embedding this into their own pricing processes.

From Risk Models to Business Decisions

RAROC is where the analytical chain from Articles 1 to 3 stops being abstract and becomes operational.

PD, LGD, and EAD feed Expected and Unexpected Loss. Unexpected Loss defines capital consumption. Capital consumption defines the denominator of RAROC. The numerator, risk-adjusted revenue, reflects pricing, fees, funding costs, and operating expenses.

When RAROC is visible at the transaction level, it changes the nature of credit discussions:

Weak structures are exposed, their capital cost is no longer invisible

Long maturities reveal their true price, they inflate Unexpected Loss non-linearly

Collateral quality becomes economically meaningful, not just a security comfort

Pricing decisions become factual rather than negotiated by feel

RAROC does not say no to risk. It asks whether risk is priced and structured honestly.

▌ The executive question

In your institution, does the credit committee review RAROC before approval, or review it afterwards to explain performance?

The Four Real Levers of RAROC

RAROC rarely improves by simply raising interest rates. It improves because decisions get smarter. In practice, four levers matter most.

1. Structure and Maturity

Long maturities increase exposure to uncertainty and inflate capital requirements. Shortening tenor often improves RAROC more than repricing ever could, and it does so without increasing the nominal cost to the borrower.

2. Collateral Quality

Better collateral reduces LGD, lowers Unexpected Loss, and directly frees capital. This creates room for competitive pricing without sacrificing risk-adjusted profitability. It is one of the few win-win levers in credit structuring.

3. Scale and Operating Efficiency

Operating costs are largely fixed. Larger, well-structured exposures often deliver higher RAROC than small, operationally intensive loans, despite appearing riskier on the surface. This dynamic is frequently overlooked in portfolio strategy.

4. Relationship Economics

Cross-selling deposits, transaction accounts, or fee-based services improves total return without increasing capital consumption. RAROC captures this reality explicitly, and it is one of the strongest arguments for relationship banking over transactional lending. This connects directly to the ideas in our White Paper on Customer Centricity: deep client relationships are not just a service philosophy. They are a capital efficiency strategy.

“These four levers turn credit from a product into a relationship strategy.”

— Q-Lana White Paper on Credit Risk

RAROC as a Management Tool, Not a Risk Metric

Here is where most institutions miss the point. RAROC is frequently used as a post-approval reporting metric, a number calculated after the decision to explain what happened. That misses its real power entirely.

Used correctly, RAROC:

Informs approval decisions before capital is committed

Shapes product design, which structures generate value and which destroy it

Guides portfolio rebalancing toward higher-returning segments

Links frontline decisions to Board-level objectives

Aligns incentives across relationship management, credit, and finance

When RAROC is embedded in the approval process, relationship managers understand why certain deals are declined. Credit committees focus on structure, not just risk ratings. Management can see, segment by segment, where the institution is actually creating value after capital, and where it is not.

RAROC becomes a common language between business, risk, and finance. That alignment is rare, and it is powerful.

RAROC and Risk Appetite: Two Sides of the Same Coin

RAROC cannot exist in isolation. It operates within a context set by the institution’s risk appetite.

A high RAROC target implies higher pricing, tighter structuring, or acceptance of lower volume. A lower RAROC threshold implies strategic growth priorities, higher capital buffers, or greater tolerance for volatility. Neither is inherently right nor wrong; they reflect different strategic positions.

What is dangerous is misalignment: aggressive volume growth paired with conservative capital; high RAROC targets alongside weak pricing power; stated discipline with undisciplined execution. This is how institutions drift.

RAROC forces coherence between ambition and resilience. It makes risk appetite operational, not as a policy document, but as a live constraint on every transaction.

Why RAROC-Driven Institutions Lend Through the Cycle

In downturns, most institutions retreat. Not because opportunities disappear, but because capital becomes scarce, uncertainty rises, and management lacks the analytical confidence to distinguish good risk from bad risk.

Institutions that understand RAROC behave differently. They know which segments still deliver acceptable risk-adjusted returns. They know where capital is being wasted. They know which structures protect the downside without killing the upside.

As competitors pull back indiscriminately, these institutions lend selectively and often strengthen their market position in the process. RAROC does not make institutions conservative. It makes them confident under pressure.

▌ Q-Lana’s approach

RAROC is one of the areas where Q-Lana’s competency in credit risk management is most tangible. It is integrated directly into our lending platform’s pricing logic and portfolio dashboards, so institutions can see, in real time, how each decision affects capital consumption, risk-adjusted return, and portfolio resilience. The goal is not to maximize a ratio. It is to allocate scarce capital where it creates sustainable value. For teams building or refining their RAROC frameworks, our Financial Skills Campus class on Risk Appetite and RAROC provides both the conceptual grounding and practical tools to get started.

▌ Q-Lana Knowledge Resources

White Paper: Credit Risk and Risk Appetite, full RAROC worked example and sensitivity analysis in Part 1, Section 5. Download at q-lana.com.

Q-Lana Financial Skills Campus (FSC): Class 2, Risk Appetite and RAROC. Covers RAROC calculation, the four improvement levers, and embedding RAROC into credit decision workflows.

FSC Course: Risk-Based Pricing, connecting RAROC to loan structuring, product design, and relationship economics in everyday lending practice.

Q-Lana White Paper: Customer Centricity in SME and Corporate Lending, the case for relationship banking as a capital efficiency strategy.

Coming Next

If RAROC tells us whether individual decisions create value, the final question becomes: how do we ensure thousands of daily decisions collectively move the institution in the right direction? That is answered by the Risk Appetite Framework, and it is the subject of our final article.