The Bridge Between Knowing and Doing

Risk appetite is the bridge between measurement and management.

The analytical chain established in this series, PD, LGD, EAD, Expected Loss, Unexpected Loss, capital allocation, RAROC, provides precision about what risk is and what it costs. But numbers alone do not steer portfolios. People do. Institutions do. And institutions need a framework that translates analytical precision into managerial intent.

A functioning Risk Appetite Framework answers questions that spreadsheets cannot:

How much volatility are we willing to absorb, and what happens when we approach that limit?

Which risks are we willing to take, and which are categorically off the table?

What level of risk-adjusted return do we require before committing capital?

Where should growth be encouraged, and where should it be slowed or stopped?

Without explicit answers to these questions, institutions do not manage risk appetite. They inherit it, from competitive pressure, from incentive structures, from the accumulated weight of decisions made without a clear framework.

What a Real Risk Appetite Framework Does

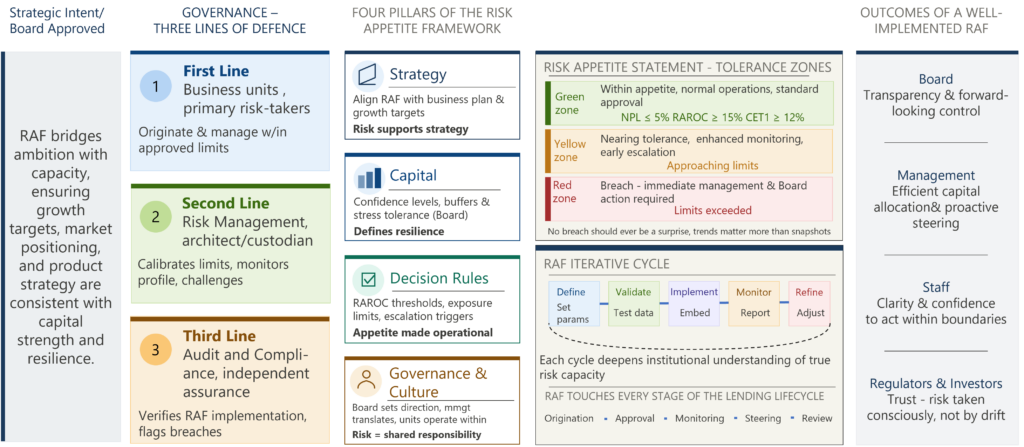

A well-designed RAF aligns four dimensions, and all four must be present for the framework to function.

Strategy

Risk appetite starts with ambition. Growth targets, market positioning, and product focus imply risk whether or not that risk is acknowledged. A bank targeting SME lending in emerging markets has a fundamentally different risk profile than one focused on investment-grade corporate credit. The RAF must make those differences explicit and ensure that ambition is consistent with capital strength and resilience.

Capital

Risk appetite is inseparable from capital planning. The choice of confidence levels, capital buffers, and stress tolerance defines how much uncertainty the institution can survive without destabilizing outcomes. This is not a finance function decision or a risk function decision. It is a Board decision, because it defines the institution’s fundamental resilience.

Decision Rules

Appetite becomes real only when it shapes approvals, pricing, and structures. Minimum RAROC thresholds, exposure and concentration limits, tenor standards, collateral requirements, escalation triggers, these are the mechanisms through which an abstract appetite statement becomes operational behavior.

Governance and Culture

A RAF works only when ownership is unambiguous. The Board sets direction. Management translates it into limits and incentives. Business units operate within defined boundaries. Risk functions monitor and challenge. Audit provides independent assurance. When this chain of accountability is clear, risk appetite governs behavior. When it is blurred, it governs documents.

▌ The governance question

In your institution, can every relationship manager explain, in plain language, what ‘within risk appetite’ means for their next credit decision?

Limits Are Necessary But Not Sufficient

Many institutions believe that setting limits is equivalent to managing risk appetite. It is not.

Limits that are hit too late offer no warning. Limits that are routinely exceeded through exception approvals offer no constraint. Concentration that builds quietly beneath individual limits offers no visibility until it is too late.

A modern RAF combines quantitative thresholds with early-warning indicators and management judgment. It recognizes that being close to a limit matters, not just breaching it. Those trends matter more than snapshots. That context matters as much as compliance.

The goal is not to prevent every breach. It is to ensure that no breach is a surprise.

“The goal is not to prevent every breach. It is to ensure that no breach is a surprise.”

Making Risk Appetite Operational

A Risk Appetite Framework only delivers value when it moves from policy to practice. Operationalization means embedding the RAF within processes, systems, and behaviors, so that every credit, investment, or operational decision reflects its principles automatically, not aspirationally.

In practice, this means:

Approval systems that show capital consumption and RAROC at the point of decision, not in the post-approval review

Portfolio dashboards that compare actual risk profiles against defined appetite in real time

Escalation paths that trigger early discussion, not late reaction

Incentive structures aligned with risk-adjusted outcomes, not raw volume

Training that gives every business unit a shared understanding of what ‘within appetite’ means for their specific role

When Appetite is Genuinely Operationalized, the Culture Shifts

Relationship managers understand trade-offs rather than resenting limits. Credit committees focus on structure and economics rather than just risk ratings. Management sees where capacity is under- or over-used. Boards gain forward-looking control, not backward-looking comfort.

Risk Appetite as a Strategic Lever

The most mature institutions use the RAF proactively, not as a defensive control but as a tool for competitive strategy.

They use it to reallocate capital toward higher risk-adjusted opportunities when markets shift. To adjust growth targets dynamically as conditions change. To protect resilience while competitors retreat into risk aversion. To enter new markets deliberately, having assessed the risk against their capacity, rather than opportunistically.

The RAF is not about restriction, but freedom with discipline.

Institutions with a clear, operational risk appetite can say yes with confidence, and no without regret. Both are powerful.

The institutions that grow sustainably over the cycle are not those with the most sophisticated models. They are the ones that align ambition with capacity, growth with resilience, and analytics with governance.

The Role of Technology: From Framework to System

Risk appetite cannot be managed effectively on spreadsheets and PDF documents. That is not a technology opinion, it is a governance reality. Manual processes create latency. Latency creates risk.

To function in real time, the RAF must be digitized:

Limits configured in systems, not described in documents

Exposures monitored continuously, not reviewed monthly

Breaches flagged automatically, not discovered in committee

Decisions documented transparently, creating audit trails and institutional memory

Digitization does not replace judgment. It ensures that judgment is exercised before risk accumulates, and that the institution learns from every decision it makes.

▌ Q-Lana’s approach

Risk appetite is not a framework we advise on from the outside. It is a competency we have built into the architecture of our platform and the curriculum of our Financial Skills Campus. At Q-Lana, capital, RAROC, limits, and early-warning indicators operate as a single integrated system, so appetite is enforced not by reminders, but by design. The platform turns the RAF from a governance document into a live management tool. And the FSC ensures that the people using it understand not just how to operate the system, but why it matters.

Closing the Loop on This Series

This series has traced a complete chain, from the fundamental variables that define credit risk to the strategic framework that governs how risk is taken across an institution.

Expected Loss explains the average cost of risk

Unexpected Loss defines the capital needed to survive when averages fail

Capital allocation at the loan level ensures that volatility is visible before it accumulates

RAROC tests whether returns justify the capital committed

Risk Appetite ensures that all of this adds up to strategy, not accident

Remove any one element, and the system becomes unreliable. Include all five, embed them in systems and culture, and risk management becomes what it should always have been: not a defensive function, but the foundation for sustainable, confident growth.

This is the thesis that runs through all of Q-Lana’s work, our platform, our advisory practice, our Thought Leadership Series, and our Financial Skills Campus. Credit risk management is not a compliance obligation. It is a core institutional competency. And like any competence, it improves with investment, practice, and the right tools.

“Risk does not limit growth. Unstructured risk does.”

— Q-Lana White Paper on Credit Risk

When risk appetite is clear, capital is disciplined, and returns are risk-adjusted, institutions do not drift. They steer.

▌ Q-Lana Knowledge Resources

White Paper: Credit Risk and Risk Appetite, the full RAF design, Risk Appetite Statement structure, and Q-Lana’s digitalization approach are covered in Part 2. Download at q-lana.com.

Q-Lana Financial Skills Campus (FSC): Class 2, Risk Appetite Frameworks. Covers RAF design principles, the Risk Appetite Statement, operationalization, and governance.

FSC Connected Curriculum: Portfolio Steering, Capital Optimization, and Credit Culture, courses that connect the RAF to everyday decisions across the lending lifecycle.

Q-Lana Thought Leadership Series: Three papers on Data Management, Customer Centricity, and Credit Risk Management, a connected view of responsible financial institution management. All available at q-lana.com.