Expected Loss (EL) represents the average level of credit losses a financial institution anticipates over a given time horizon, typically one year. It quantifies the cost of bearing credit risk and is a foundational concept in pricing loans, setting provisions, and managing portfolios. The formula for calculating Expected Loss is:

Each component (Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD)) provides a distinct perspective on risk, and their combination offers a comprehensive view of expected credit loss.

What Is Expected Loss (EL)?

Expected Loss is a cost. It is comparable to an insurance premium. Just as insurance companies calculate premiums to cover anticipated claims, financial institutions use EL to estimate the average losses they might incur from defaults in their loan portfolios.

EL = PD × LGD × EAD

Expected Loss in Loan Loss Provisions

Expected loss allows financial institutions to:

1. Calculate Provisions and Reserves:

EL guides the allocation of provisions to ensure the institution is prepared for average losses. These reserves act as a buffer against expected defaults, ensuring the institution remains solvent and operational.

2. Calculate Loan Pricing:

EL influences loan pricing, as it represents the cost of credit risk. For example, if the calculated EL for a loan is $100, this amount must be factored into the loan’s interest rate or fees to ensure adequate compensation for the risk.

3. Risk Management:

Institutions use EL to monitor portfolio health. If EL increases due to rising PDs or LGDs, it may signal deteriorating credit quality or external economic pressures, prompting preemptive action

Limitations of Expected Loss

EL, however, is not an indication of risk and uncertainty. It does not account for variability or extreme outcomes, which are addressed by Unexpected Loss (UL).

Calculating Expected Loss Step By Step

Examples

Some examples will help understanding the dynamics of the Expected Loss. Consider a loan portfolio consisting of 100 homogenous loans. Each loan has the following characteristics:

- Loan amount (face value at disbursement): $10,000

- Term: 4 years, linear amortization

- Probability of Default (PD): 5%

- Collateral Value: $3,000

- Default Timing: The default event happens on average after 2 years.

Calculating EL for an Individual Loan

We calculate the Expected Loss (EL) for an individual loan:

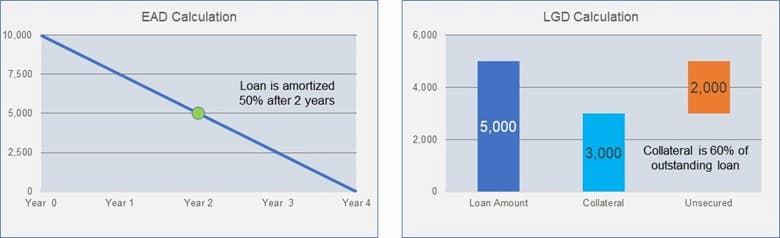

- Step 1: Estimate EAD

Estimate Exposure at Default (EAD): Given the linear amortization, the exposure at the midpoint (two years) is 50% of the original loan amount:

EAD = 0.5 × 10, 000 = 5, 000

- Step 2: Estimate LGD

Estimate Loss Given Default (LGD): With a collateral value of $3,000 against an exposure of $5,000, the lender will lose $2,000, thus, the LGD is 40%.

Using the input to calculate, the Expected Loss for a single loan results in $100

EL (Individual Loan) = 10, 000 × 5% × 40% × 50% = 100

What is the actual loss if one loan defaults?

This question differs from the EL calculation because it assumes that the borrower has already defaulted removing the probability component. For a loan amount of $10,000, an EAD of 50% ($5,000), and an LGD of 40%, the loss is:

Loss in Default = 10, 000 × LGD × EAD = 10, 000 × 40% × 50% = 2,000

The actual loss if one loan defaults is $2,000, irrespective of the probability of default.

What is the expected loss of the total portfolio?

We know that there are 100 homogeneous loans in the portfolio. The EL for an individual loan is $100. Multiply by the total number of loans in the portfolio:

EL (Portfolio) = EL (Individual Loan) × 100 = 10, 000

The total expected loss for the portfolio is $10,000.

What Happens When Reality Deviates from Expectations

While Expected Loss provides an average estimate, real-world defaults often deviate from expected values due to their probabilistic nature. Let us explore two scenarios where the actual default rate differs from the expected 5%.

Scenario 1: Fewer Defaults Than Expected (4%)

If only 4% of loans default instead of 5%, the number of defaults in a portfolio of 100 loans is 4. The loss per defaulted loan is $2,000 (as calculated earlier), so the total loss is:

4 × 2, 000 = 8, 000

With provisions of $10,000 set aside, the institution has a surplus of $2,000, which could be retained as additional reserves. However, in many cases, institutions may treat this surplus as profit, distributing it as dividends or bonuses to shareholders and staff.

Scenario 2: Higher Defaults Than Expected (6%)

If the default rate increases to 6%, the number of defaults in the portfolio is 6. The total loss increases to:

6 × 2, 000 = 12, 000

In this case, the institution’s provisions of $10,000 fall short by $2,000. This shortfall must be covered by equity capital, underscoring the importance of maintaining an adequate capital buffer to absorb such unexpected losses.

What Causes Deviations in Portfolio Losses?

Real-world portfolios rarely conform strictly to expected default rates. Variability can arise from factors such as:

- Economic Conditions: During recessions, defaults tend to increase, while strong economic growth may reduce default rates.

- Model Accuracy: Poor calibration of Probability of Default (PD) or other variables can lead to skewed projections.

- Default Range: If defaults range from 3% to 7%, portfolio losses would vary between $6,000 and $14,000. Such variability underscores the importance of robust provisioning strategies and regular stress testing.

Complex Portfolios

How Do You Deal With Them?

In addition to these variations, there are other aspects to consider in a more complex assessment

- Heterogeneous Portfolios: For portfolios with diverse loan structures, collateral types, or borrower profiles, EL must be calculated for each loan or segment and then aggregated.

- Dynamic LGD and EAD: Factors like collateral depreciation, legal delays, or unexpected drawdowns can alter LGD and EAD over time, requiring regular reassessment.

- Correlation Effects: While EL assumes independent defaults, real-world portfolios often exhibit correlation (e.g., defaults clustering during economic downturns). Though EL itself does not account for these dynamics, it is a key input for more complex risk models, including stress tests and scenario analyses.

Bridging to Unexpected Loss

Expected Loss gives you the average, but not the whole picture. The financial institution must also account for Unexpected Loss (UL), which captures variability and ensures capital adequacy during periods of higher-than-expected defaults.

Q-Lana Calculates Expected Loss and Unexpected Loss Automatically

- At both the loan and portfolio level, and feeds the results directly into RAROC and risk appetite reporting.

In the next chapter, we explore how UL builds on EL to provide a comprehensive view of credit risk and inform decisions on capital allocation.