Q-Lana has integrated the Business Model Canvas (BMC) within its Loan and Asset Management System to help financial institutions better assess SME customers. This integration allows loan officers to systematically capture key elements of an SME’s business model within the lending workflow. By mapping out customer segments, value propositions, and revenue streams directly within the platform, financial institutions can gain deeper insights into a client’s business dynamics.

Using Business Model Canvas to Identify Risks and Opportunities

The tool also enables real-time identification of potential risks and opportunities, which enhances the credit analysis process and improves decision-making outcomes. Additionally, this structured approach helps ensure that loan officers provide more tailored and impactful financial solutions to SME clients. By embedding the BMC into the platform, Q-Lana enables users to capture critical business insights, identify potential risks, and explore opportunities in real-time, thus enhancing the decision-making process.

Assessing SME Viability with the Business Model Canvas

For financial institutions, particularly those engaged in SME lending, the BMC can serve as a powerful tool to assess the viability and sustainability of an SME customer’s business model. This article outlines the structure of the BMC, explains how to conduct a Business Model Canvas assessment, and explores the benefits and criticisms of the tool.

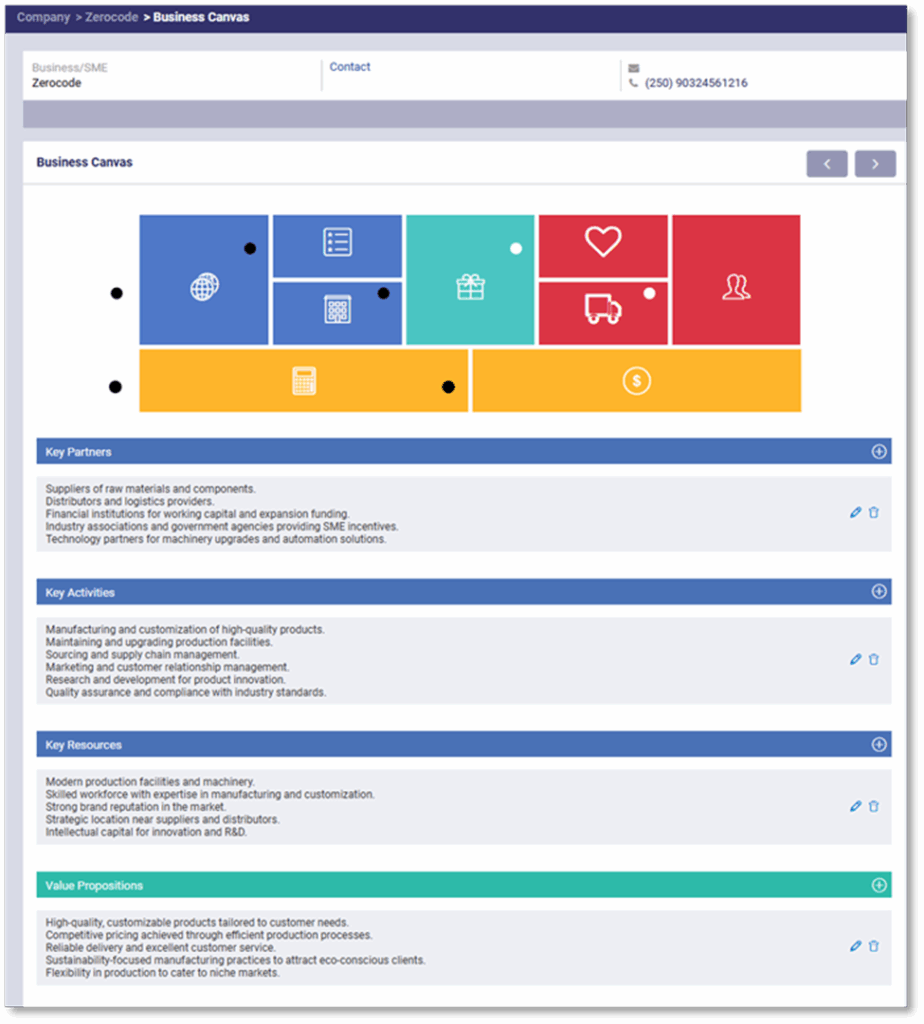

The Building Blocks of the Business Model Canvas

The BMC comprises nine interconnected building blocks that outline the essential components of a business model: These building blocks not only provide a comprehensive view of a business but also help identify both opportunities and risks. This makes the BMC a valuable risk management tool in credit analysis, as it enables financial institutions to better assess the strengths and vulnerabilities of an SME’s business model.

1. Customer Segments

Identifies the groups of people or organizations a business aims to serve.

2. Value Propositions

Describes the unique products and services offered to meet the needs of the target segments.

3. Channels

Details the ways in which a company delivers its value proposition to customers.

4. Customer Relationships

Specifies the types of relationships a company establishes with its customer segments.

5. Revenue Streams

Defines the sources of revenue generated from each customer segment.

Key Resources – Lists the assets essential to delivering the value proposition.

Key Activities – Outlines the critical actions a company must take to operate successfully.

Key Partnerships – Identifies the external companies or suppliers that help the business operate.

Cost Structure – Describes the costs involved in operating the business model.

For financial institutions, using the BMC allows for a deeper understanding of an SME’s operations, risk profile, and potential for growth.

Business Model Canvas Assessment

Conducting a Business Model Canvas requires discipline and structure, but when applied consistently, it becomes second nature for loan officers. Based on industry best practices, here is how we recommend approaching it:

Step 1: Identify Customer Segments

Determine the primary customer groups the SME serves. Segmenting customers by their needs and behaviors provides insights into the sustainability of the SME’s revenue base.

Step 2: Define the Value Proposition

Analyze what unique value the SME provides to its customers. Understanding the value proposition helps assess the SME’s competitive advantage and its ability to retain customers.

Step 3: Map the Channels

Evaluate how the SME delivers its products or services to customers. Channels can include physical stores, online platforms, or third-party distributors. Efficient channels contribute to customer satisfaction and sales growth.

Step 4: Assess Customer Relationships

Review the type of relationships the SME has with its customers. These can range from personal interactions to automated self-service models. Strong relationships often lead to customer loyalty.

Step 5: Examine Revenue Streams

Identify the SME’s revenue sources and analyze their stability and diversity. A diversified revenue stream reduces dependency on a single customer or product.

Step 6: Analyze Key Resources

Determine the critical resources the SME needs to deliver its value proposition. These can include physical assets, intellectual property, financial resources, and human capital.

Step 7: Outline Key Activities

Review the core activities required for the SME to operate effectively. This may include production, marketing, sales, or customer support.

Step 8: Identify Key Partnerships

Assess the SME’s relationships with suppliers, distributors, and other partners. Partnerships can optimize operations and reduce risk.

Step 9: Understand the Cost Structure

Evaluate the costs associated with running the SME’s business model. This includes both fixed and variable costs. Understanding the cost structure helps in assessing the financial sustainability of the SME.

Benefits of Using the Business Model Canvas

The Business Model Canvas (BMC) provides a practical way for financial institutions to evaluate SMEs beyond financial statements by highlighting how their businesses actually work.

Key Advantages of the Business Model Canvas

Holistic View – The BMC provides a comprehensive overview of the SME’s business model, making it easier to identify strengths, weaknesses, opportunities, and risks.

Simplicity and Clarity – The visual format of the BMC simplifies complex business concepts, making it accessible for both financial institutions and SME owners.

Enhanced Communication – The BMC fosters better communication between financial institutions and SME customers by providing a common framework for discussion.

Focus on Value Creation – By emphasizing value propositions, the BMC helps financial institutions assess the SME’s potential to create and capture value.

Dynamic and Flexible – The BMC can be updated as the business evolves, allowing for continuous improvement and adaptation.

Creating a Knowledge Repository for Smarter Credit Decisions

Overall, we see great value in the BMC’s ability to build a library of business cases. This library can serve as a powerful reference tool for loan officers and credit analysts, improving the consistency and quality of credit assessments over time. By comparing various customer cases, financial institutions can identify patterns, learn from past experiences, and make more informed lending decisions. It also enhances knowledge sharing within the institution, fostering a deeper understanding of different business models and their associated risks and opportunities. This will help the staff of a Financial Institution to learn about business models and compare various customers against each other

Criticisms of the Business Model Canvas

The BMC is also criticized for some aspects

Lack of Depth – The BMC provides a broad overview but may lack the depth needed for detailed financial analysis.

Focus on Existing Models – The BMC is more effective for analyzing existing business models rather than developing new, disruptive ones.

Assumption of Stability – The BMC assumes a relatively stable environment, which may not be realistic in rapidly changing markets.

Over-simplification – The visual simplicity of the BMC can sometimes lead to an oversimplification of complex business dynamics.

While the BMC is a valuable tool, it is not without its limitations: Despite these criticisms, we believe that the Business Model Canvas is an excellent tool to systematically understand the business model of an SME. We have often observed that loan officers, due to time constraints, do not fully grasp all aspects of a customer’s business, which results in suboptimal support for the client. By using the BMC, loan officers can gain a more structured and comprehensive understanding of the SME’s operations, enabling them to provide better advisory services and tailor financial solutions more effectively. For instance, a loan officer working with a small retail business can use the BMC to identify that the business’s primary challenge lies in its distribution channels. By recognizing this issue, the loan officer can suggest tailored financial products such as a working capital loan to improve supply chain efficiency or offer advice on expanding digital sales channels, thereby providing more targeted and impactful support.

Building Better SME Credit Assessments

The Business Model Canvas is a practical and versatile tool that financial institutions can use to assess SME customers. By systematically analyzing the nine building blocks, financial institutions gain valuable insights into the SME’s business operations, strengths, and risks. Despite some criticisms, the BMC remains a popular framework for business model analysis due to its simplicity and focus on value creation. For financial institutions, particularly those operating in developing markets, the BMC offers unique value by providing a structured approach to understanding the complexities of SMEs. It helps lenders uncover both opportunities and risks, ensuring a more comprehensive credit analysis that can foster better lending decisions and stronger client relationships. For financial institutions, integrating the BMC into their SME assessment process can lead to more informed lending decisions and stronger client relationships.