What We Covered

Chapter 1: PD, LGD, and EAD

PD, LGD, and EAD are Foundational Risk Variables

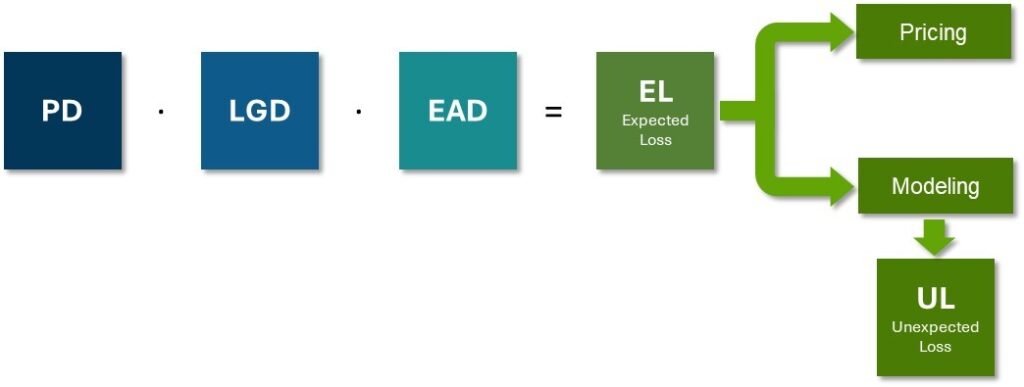

We begin the credit risk series by examining the three foundational variables:

i. Probability of Default (PD)

ii. Loss Given Default (LGD)

ii. Exposure at Default (EAD)

These three metrics form the foundation of credit risk quantification, providing a common language for pricing, provisioning, and regulatory compliance.Chapter 2: Expected Loss (EL)

The Concept of EL and UL

We then introduce the concepts of Expected Loss and Unexpected Loss, and how the latter plays a central role in determining capital adequacy. These principles form the basis for understanding regulatory capital frameworks, such as those outlined under the Basel Accords, and practical tools like Risk-Adjusted Return on Capital (RAROC) for performance measurement.

Throughout this publication, we aim to balance analytical rigor with practical clarity. Even the more advanced concepts are presented in a way that makes them accessible and actionable for professionals involved in day-to-day credit risk management. The Q-Lana Loan and Asset Management Platform is designed to integrate these concepts into institutional processes, supporting the operationalization of sound credit risk practices. In addition, our advisory services help institutions customize and implement these methodologies in alignment with their strategic objectives.

Chapter 3: Unexpected Loss (UL)

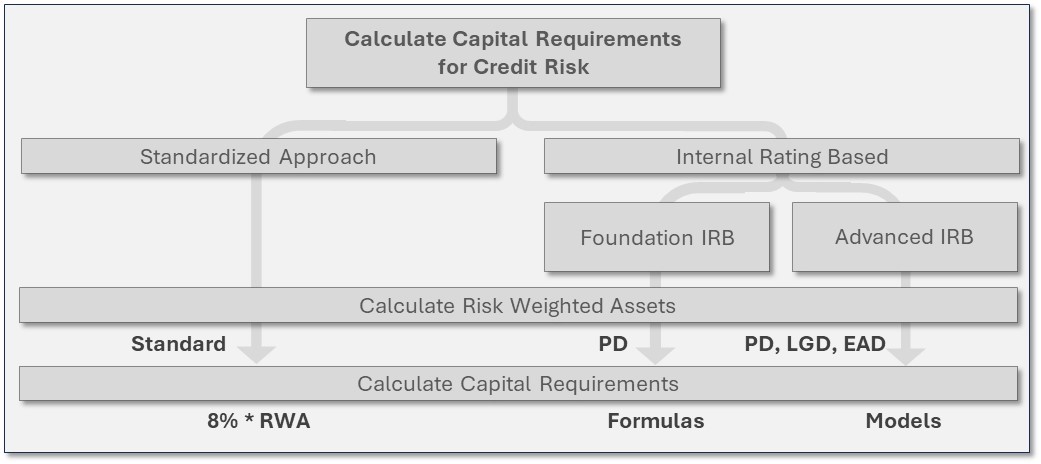

Chapter 4: Capital Requirements per Loan

Chapter 5: RAROC

Main Learnings from the Credit Risk Series

i. Credit Risk Concepts Vs Performance and Pricing

This concept note has outlined the fundamental principles of credit risk management and pricing, beginning with the core elements (Expected Loss (EL) and Unexpected Loss (UL)) and extending to their practical application in loan pricing, capital allocation, and financial performance management.

ii. PD, LGD, and EAD Drive Risk Quantification

We explored the role of Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD) as critical drivers of credit risk quantification. These variables serve as the foundation for calculating both EL and UL, enabling institutions to provision for average losses and reserve capital for more volatile outcomes. We then translated these risk calculations into actionable strategies through the Risk-Adjusted Return on Capital (RAROC) framework—a powerful tool for evaluating whether a loan’s return is sufficient for the capital it consumes.

iii. Risk Models Can be Integrated into Daily Decision-Making

Throughout this publication, we emphasized the importance of integrating risk models into daily decision-making, allowing financial institutions to steer portfolios more effectively, price products more accurately, and achieve stronger, risk-aligned profitability.

Q-Lana’s Platform

At Q-Lana, we recognize that implementing a robust credit risk framework, especially one incorporating RAROC, requires more than theory. It demands the right tools, structured methodologies, and collaborative execution.

i. Technology That Enables Credit Risk Strategy

Our Loan and Asset Management Platform is designed to support this transformation. Built on low-code architecture and configured to align with institutional needs, Q-Lana’s platform offers:

- Fully integrated modules for PD, LGD, and EAD analysis

- Real-time EL and UL monitoring across loans and portfolios

- Automated pricing logic using RAROC principles

- Comprehensive reporting to meet both internal and regulatory standards

ii. Implementation as a Partnership, Not a Product

Just as important as technology is the partnership behind it. Implementing RAROC and advanced credit risk practices involves aligning methodologies, configuring systems, and training staff to make the most of these tools. At Q-Lana, we thrive on this process. We work closely with financial institutions to ensure that risk management isn’t just a compliance function—but a strategic capability that drives sustainable growth.

Let’s Help you Transform Credit Risk Management

Whether you are just beginning your journey toward risk-based pricing or looking to enhance your current framework, we’re here to support you.

We help you transform credit risk management into a powerful engine of profitability, resilience, and competitive advantage..