Porter’s 5 Forces Model, developed by Michael E. Porter, is a strategic tool that helps businesses analyze the competitive dynamics of their industry. For financial institutions lending to Small and Medium Enterprises (SMEs), this model can be a valuable framework to assess the competitive position of potential borrowers. By understanding the forces shaping the market, lenders can make more informed decisions, anticipate risks, and identify growth opportunities for borrowers.

Q-Lana’s Loan and Asset Management Platform includes a built-in Porter’s 5 Forces Tool that integrates seamlessly with other features such as financial analysis modules, risk assessment tools, and portfolio management functionalities. This integration allows financial institutions to leverage the model for both sector assessments and borrower evaluations in a more comprehensive manner. The Porter’s 5 Forces Tool supports analysts in understanding industry-specific competitive dynamics, identifying key risks and opportunities, and tailoring lending strategies to better match the unique challenges of each sector. Additionally, by embedding this tool within the platform, users can regularly update their assessments, ensuring that the insights remain relevant and actionable over time.

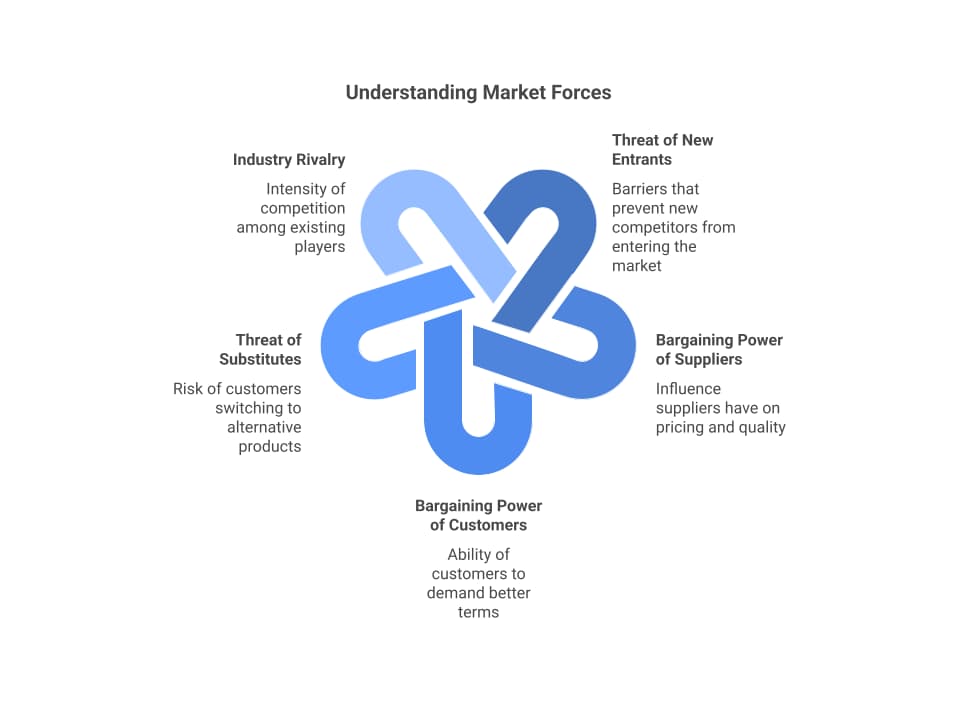

Understanding Porter’s 5 Forces Model

Porter’s 5 Forces Model identifies five key forces that influence the competitiveness of an industry:

1. Threat of New Entrants:

This refers to the ease with which new competitors can enter the market and disrupt existing businesses. High barriers to entry, such as significant capital requirements or regulatory restrictions, reduce this threat. For example, in the renewable energy sector, entering the market often requires substantial investment in infrastructure, regulatory approvals, and specialized expertise. SMEs in this sector may face challenges in securing the necessary funding to set up solar farms or wind energy projects. These barriers create a protective moat for established players while making it difficult for new entrants to compete effectively.

2. Bargaining Power of Suppliers:

Suppliers can exert pressure on businesses by increasing prices or reducing the quality of goods and services. The power of suppliers is higher when there are fewer suppliers or when switching costs are high. For example, a small café relying on a unique coffee bean supplier may face significant pressure if that supplier decides to increase prices or alter terms. Since switching to a new supplier could affect the taste and quality of their products, the café has limited bargaining power, making it highly dependent on maintaining that supplier relationship.

3. Bargaining Power of Customers:

Customers’ ability to demand lower prices or better services influences a business’s profitability. For example, a small furniture manufacturer that relies heavily on contracts with a few large retailers may experience significant pressure to lower prices or meet specific quality requirements. If those retailers have numerous alternative suppliers, they can leverage their bargaining power to negotiate better terms, making it challenging for the SME to maintain profitability. This power increases when customers have many alternatives or when products are undifferentiated.

4. Threat of Substitutes:

This force measures the risk of customers switching to alternative products or services. For example, a local bakery may face competition from grocery chains that offer similar baked goods at lower prices. Customers may find the convenience and pricing of grocery chains more appealing, which increases the threat of substitution. The bakery must differentiate itself through unique offerings or superior quality to retain its customer base. The threat is higher when substitutes offer better value or are more affordable.

5. Industry Rivalry:

The intensity of competition among existing players in the market affects profitability. High rivalry is characterized by numerous competitors, slow industry growth, and low product differentiation.

The five forces analysis provides a comprehensive view and insights focused on profitability and has universal applications across industries. However, it is important to recognize that the model has certain limitations. For instance, it is often criticized for being static in nature and may not account for rapidly changing market dynamics. Additionally, the model lacks the quantification of factors, which can make it challenging for SMEs to apply effectively. Despite these limitations, it remains a useful tool to enhance credit risk analysis by structuring the analyst’s thinking and providing valuable sector assessments that can be applied across multiple companies.

Conducting a Porter’s 5 Forces Assessment for SME Borrowers

Understanding the competitive position of SME borrowers is crucial for financial institutions to evaluate credit risk effectively. Conducting a Porter’s 5 Forces assessment allows lenders to gain deeper insights into the external market forces impacting a borrower’s business, helping them anticipate potential challenges and opportunities in various sectors.

When assessing an SME borrower using Porter’s 5 Forces, financial institutions should:

1. Analyze the Threat of New Entrants

- Evaluate the ease with which competitors can enter the borrower’s market.

- Identify barriers to entry such as regulatory requirements, capital investment, brand loyalty, and economies of scale.

- Determine how vulnerable the borrower’s business is to new competition.

2. Assess the Bargaining Power of Suppliers

- Identify key suppliers and evaluate their importance to the borrower’s operations.

- Determine the availability of alternative suppliers and the costs associated with switching.

- Assess whether suppliers can influence prices or the availability of crucial inputs.

3. Evaluate the Bargaining Power of Customers

- Identify the borrower’s customer base and their ability to negotiate prices or terms.

- Determine if customers have alternative options or if they are dependent on the borrower’s products/services.

- Assess the level of customer loyalty and the cost of customer acquisition.

4. Examine the Threat of Substitutes

- Identify potential substitute products or services that could replace the borrower’s offerings.

- Assess the price-performance trade-off of substitutes.

- Determine how easily customers can switch to alternatives and what impact that would have on the borrower’s business.

5. Review Industry Rivalry

- Identify the borrower’s direct competitors and their market share.

- Assess the intensity of competition in the borrower’s industry.

- Evaluate the borrower’s differentiation strategy and competitive advantage.

Benefits of Using Porter’s 5 Forces Model

The application of Porter’s 5 Forces Model offers several benefits for financial institutions assessing SME borrowers:

1. Comprehensive Market Understanding:

It provides a holistic view of the borrower’s industry dynamics, helping lenders understand the challenges and opportunities the business faces.

2. Risk Identification:

The model helps identify external risks that could impact the borrower’s profitability and stability.

3. Informed Decision-Making:

By understanding competitive pressures, lenders can make more informed credit decisions and set appropriate loan terms.

4. Proactive Risk Management:

The insights gained from the model can help lenders anticipate changes in the borrower’s market and take proactive measures to mitigate risks.

Challenges of Using Porter’s 5 Forces Model

While the model is a valuable tool, it also presents some challenges:

1. Complexity of Data Collection:

Gathering accurate and comprehensive data about the borrower’s industry can be time-consuming and challenging.

2.Dynamic Market Conditions:

The forces in the model are not static; they change over time. Regular updates to the assessment are necessary to maintain relevance.

3. Subjectivity in Analysis:

The interpretation of the forces may vary based on the analyst’s perspective, leading to potential biases.

4. Limited Quantification:

The model does not provide a quantitative approach to measuring the impact of each force, which can be a drawback for SMEs with limited resources.

To overcome these challenges, financial institutions can leverage digital tools like Q-Lana’s Loan and Asset Management Platform, which integrates real-time insights into its Porter’s 5 Forces Tool. By using Q-Lana, institutions can enhance their sector assessments by dynamically analyzing competitive pressures that impact their SME clients. The tool helps lenders identify key risks and opportunities within the industries their borrowers operate in, leading to more informed credit decisions and customized lending strategies. Additionally, the platform’s integration with other features, such as financial analysis and risk management modules, ensures a holistic approach to understanding borrower dynamics. Consulting external experts can further enhance these assessments by providing additional perspectives on industry trends and competitor behavior, enabling financial institutions to adapt their strategies and support SME borrowers more effectively.

Conclusion

Porter’s 5 Forces Model is a powerful tool for financial institutions to assess the competitive position of SME borrowers. By analyzing the market dynamics and identifying the key forces at play, lenders can better understand the risks and opportunities associated with a borrower’s business. However, it is essential to complement this model with other analytical tools and maintain regular updates to account for changing market conditions. When used effectively, Porter’s 5 Forces can significantly enhance a lender’s ability to make informed credit decisions and support the growth and success of SME borrowers.